Inflation Is Already Impacting Consumers’ Long-Term Financial Goals

This is a preview of our latest State of Consumer Banking and Payments report.

Inflation is causing a widespread drop in financial well-being among U.S. adults, with historically disadvantaged demographics more impacted than others. In addition to short-term financial hardships, consumers are beginning to shore up their immediate finances by delaying — or scrapping altogether — their long-term financial goals.

Download the full report here.

With financial well-being already strained by the pandemic, consumers are now having to grapple with another serious setback in decades-high inflation. Amid volatile markets and waning consumer sentiment, it’s important for financial services leaders and their employees to look beyond macro indicators and understand more intimately how the average consumer translates these challenges to their financial planning and wellness. Finances increasingly dominate people’s lives, and consumers are already forsaking their long-term goals in order to stay afloat.

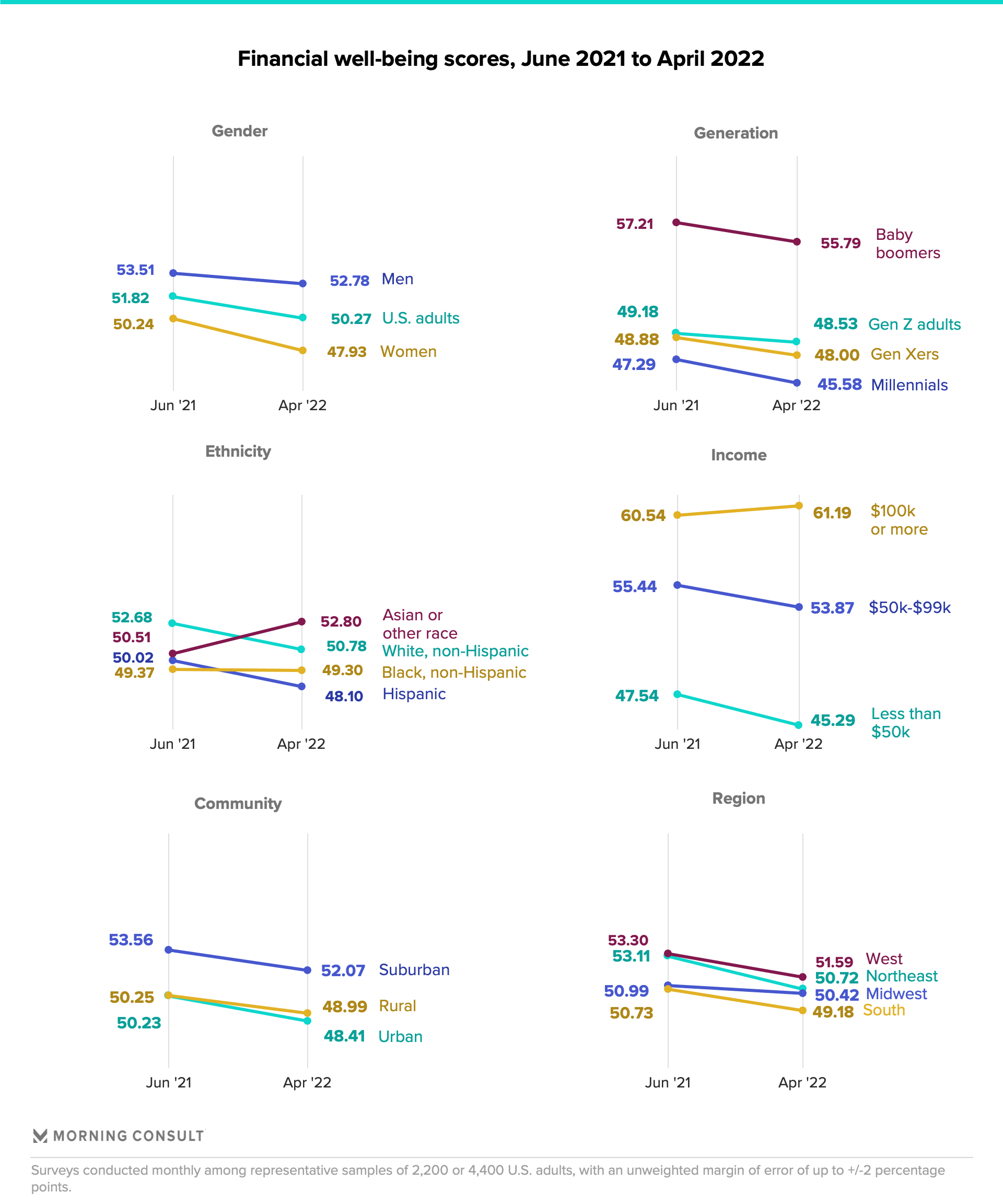

Financial well-being has dropped among almost all U.S. adults

Morning Consult’s financial well-being score, tracked monthly, is a concise and more personal way of understanding how various demographics are experiencing economic conditions over time. Since tracking began in June 2021, the financial well-being of the average U.S. adult has fallen 1.55 points (from 51.82 then to 50.27 in April), with several cohorts that were already experiencing low financial wellness in 2021 seeing more severe drops: women (down 2.31 points), households earning less than $50,000 annually (down 2.25 points) and Hispanic adults (down 1.92 points).

Even groups with traditionally higher financial well-being have seen drops, including Gen Xers, baby boomers, households earning between $50,000 and $99,999, and non-Hispanic white adults. The largest drop can be seen among those living in the Northeast region of the United States, with their scores down 2.39 points between June 2021 and April 2022.

While these score shifts may appear small, even the slightest change can be meaningful. For example, an individual’s 1-point month-over-month increase is associated with a $15,000 increase in household income or a 20-point credit score hike, per the Consumer Financial Protection Bureau, which developed the financial well-being score. As such, the 2.25-point drop for households earning less than $50,000 annually could mean an income decrease of nearly $34,000 — an unimaginable hit for consumers already weathering the economy on multiple fronts, and even more so for those with children.

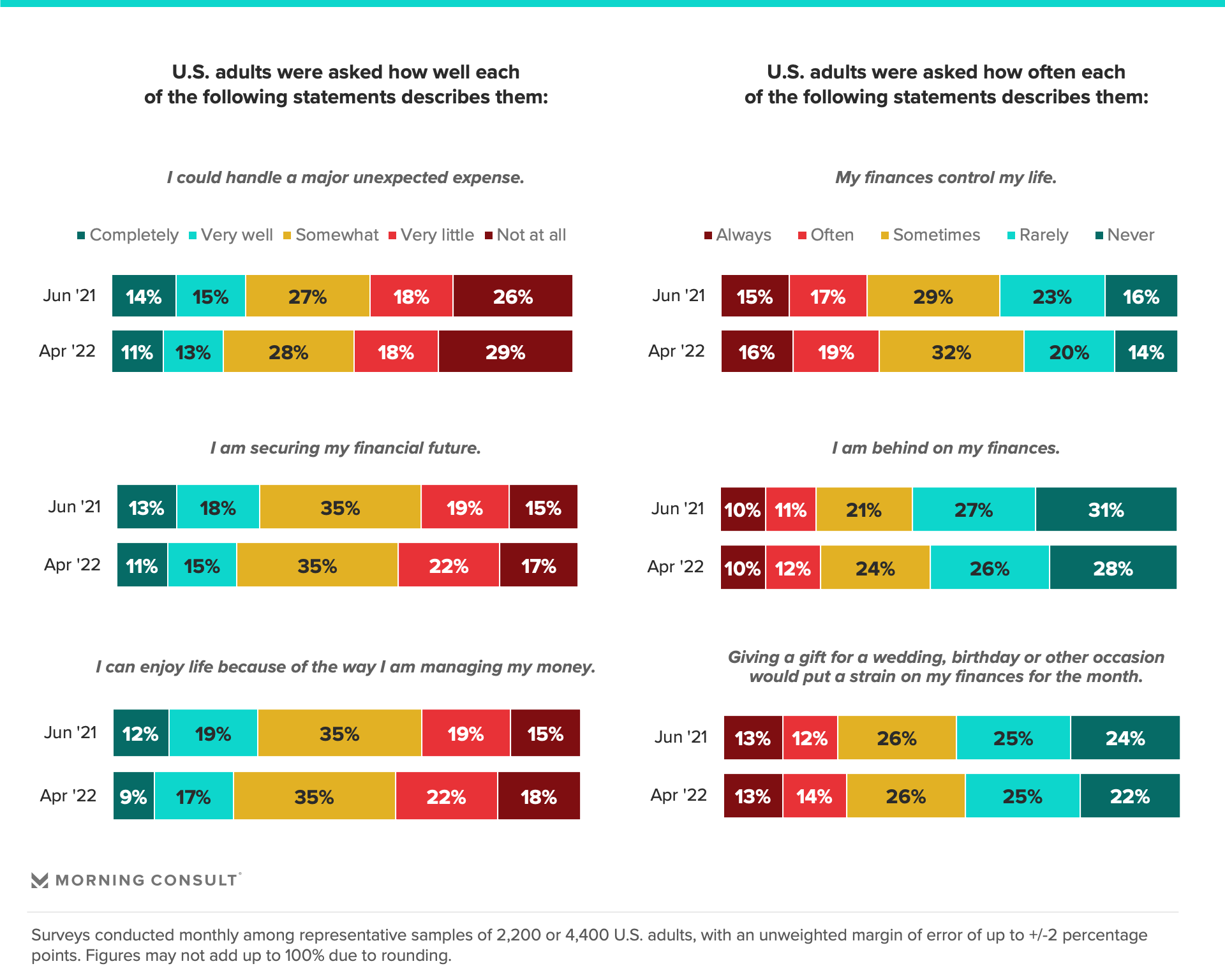

Sentiment toward personal finances is increasingly negative, reflecting present and future fears

Morning Consult’s financial well-being scores are derived from consumers’ responses to a series of 10 statements about their perspectives on how their near- and long-term finances impact their lives. Consumers’ continuously declining financial health from June 2021 to April 2022 reflects deteriorating outlooks on both: Not only are they in a tight spot financially right now and unable to enjoy life as a result, but they’re also increasingly worried about what this means for their future.

Compared with almost a year ago, a smaller share of adults in April said they could handle a major expense, and the same is true of those who said they’re able to enjoy life because of their money management. Our data also shows a diminishing share of adults who say they are “rarely” or “never” behind on their finances, which in turn impacts the share of those who say they are securing their financial future.

Cutting costs to make ends meet, consumers are having to forsake their long-term goals

Rising prices of essential goods means consumers are slashing discretionary spending, but for many this isn’t enough. Morning Consult’s economic analysis confirms that both financial vulnerability and income inequality are on the rise. As of March, the share of adults whose expenses exceed their income had jumped 3.7 points year over year, with lower-income adults suffering the most.

More worrisome still is that consumers are slowing or halting progress toward their long-term financial goals.

The shares of adults reporting that they made progress toward long-term financial goals like purchasing a home, saving for education and starting a business have each dropped 25% from June 2021 to April 2022. Consumers are clinging more tightly to their investment, retirement and emergency fund goals, which have seen drops in progress of 15%, 14% and 13%, respectively.

A deeper look reveals even more concerning drops among specific communities, such as a 20% decrease among Gen Xers reporting progress toward saving for retirement, a 35% decrease among millennials reporting progress toward saving for education and a 27% drop among Black adults reporting progress toward creating an emergency fund. Each of these findings has broad implications that do not bode well for any of these groups if inflation gives way to a full-blown recession. Gen Xers may have to put off retirement; millennials, who already have one of the lowest financial well-being scores, may not be able to upskill themselves or their dependents through further education; and Black adults, who are historically underserved by the financial services industry, will have even less of a safety net to weather the rough months ahead.

The one semi-bright spot is that consumers’ ability to maintain their budgets and improve their credit has not meaningfully changed. Prioritizing these goals becomes more difficult during times of economic uncertainty, but they’re both vital to overall financial health.

As financial services providers prepare to coach consumers through the coming months, the industry should home in on how Americans’ long-term goals are shifting to accommodate their short-term needs, and help them reprioritize their finances so they can remain afloat as headwinds mount.

Charlotte Principato previously worked at Morning Consult as a lead financial services analyst covering trends in the industry.