ESG in Retail: 6 Consumer Profiles to Know

About half of adults or more said they pay at least some attention to ethical and political matters when deciding where to shop — and a new Morning Consult analysis shows that shoppers fall into six different cohorts based on how they react to environmental, social and governance initiatives, as well as their views on company engagement with political and cultural issues. This analysis reveals that the benefit of speaking out on ESG issues is substantial, as the shoppers who disagree with these initiatives are unlikely to change their behaviors in response.

As brand leaders increasingly feel motivated — or pressured — to take a stance on a number of societal issues, the question now is whether or not ESG statements translate to changes in consumer behavior.

To provide a more concrete framework to help brands evaluate how their ESG positions may land with shoppers, Morning Consult conducted a new cluster analysis that segments cohorts based on the brand attributes that consumers value, what factors they prioritize while shopping and their likelihood to boycott (or buycott) brands that engage in various political, cultural and social issues. This analysis avoids the “say-do” pitfalls that come from asking people about hypothetical actions taken after a hypothetical situation, and the resulting clusters define which audiences want and support brands that take stands, and which audiences brands risk alienating.

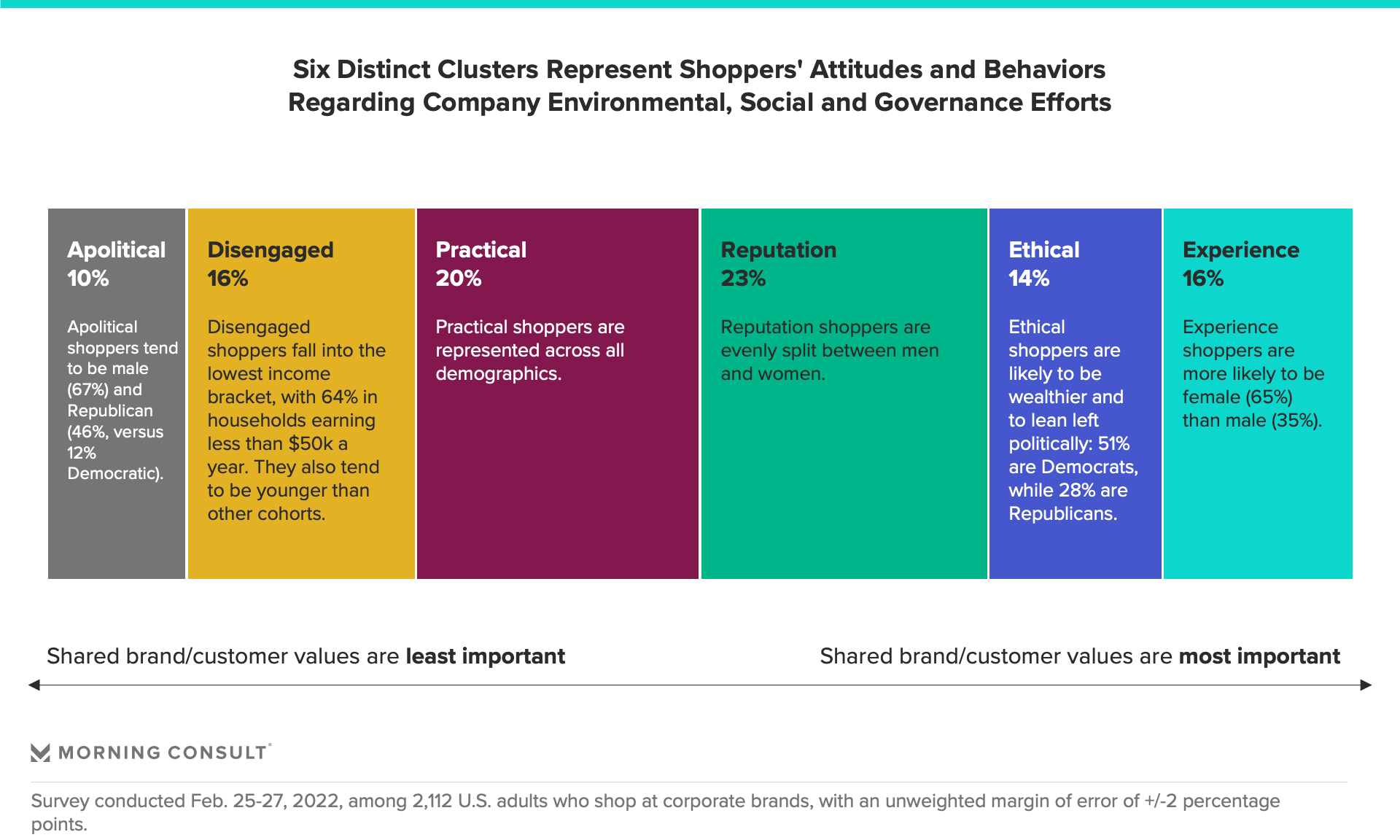

Six profiles reflect shopper attitudes ranging from apathetic to proactive

From left to right, each cohort places increasing importance on shopping from brands that have similar values to their own.

- Apolitical shoppers, who are most likely to be male and politically conservative, constitute the smallest segment and are the least interested in ESG brand traits. Rather, they tend to choose brands based on price and product availability. While shared values, brand history and reputation are decidedly not as important to this cohort, brand trust is.

- Disengaged shoppers are not only uninterested in brand stances on social issues, but they’re also indifferent to brand trust and other, more practical purchase drivers such as price. Traditional marketing levers do not appeal to this cohort. Of all six cohorts, this group contains the youngest shoppers, and trends lower on household income.

- Practical shoppers are all about getting the best bang for their buck, and are primarily driven by reasonable prices, product availability and product value. This group is unlikely to do any research on brand ethics or to change their behavior if they do find that a brand is inconsistent with their values.

- Reputation shoppers say they want the brands they shop from to be a force for societal good, but their actual behavior does not match their attitudes: They are just as likely to look the other way if a company acts unethically as they are to stop purchasing from it. This cohort exhibits the classic say-do gap common in ESG survey research — they might say they pay attention to brand statements, but they’re unlikely to modify their behavior as a result.

- Ethical shoppers — who tend to have higher household income and more politically liberal views — pay a lot of attention to company stances and policies on ethical matters, sustainability commitments and diversity, equity and inclusion commitments. This cohort is proactive about walking the walk — 3 in 4 members of this group said they have boycotted a company for political reasons in the past year, and 71% have spent money with a company as a result of its political stances. Members of this group are most likely to reward brands that align with their values, while they will punish the ones that get it wrong by changing their purchasing behavior.

- Experience shoppers are more likely than any other group to prioritize the in-person shopping experience alongside brand ethics. They want to shop from brands that sell environmentally friendly products, as well as from companies that treat their employees well — something that correlates directly with their in-store shopping experience. These shoppers, who are more likely to be female than to be male, prefer brands to limit their activism to issues that are directly related to their business.

These results show that brands stand to gain more from taking action on left-leaning issues (like supporting environmental initiatives), as those are the causes that will score points with the customers that pay attention to PR buzz but likely won’t change their behaviors and with those who are much more likely to match shopping behavior with attitudes. Meanwhile, Apolitical and Disengaged shoppers aren’t likely to be paying attention, and if they are, they probably won’t boycott because they disagree with a brand’s stance. But to truly capture the Ethical shopper cohort (and enjoy a halo with Experience and Reputation shoppers), statements and vague promises are unlikely to suffice: Initiatives should have real reportable metrics behind them.

Want to learn more about machine-learning techniques?

Morning Consult’s data scientists used machine-learning techniques to train a model on a subset of this data that can predict cluster membership in new data sets. To learn more about how this typing tool can be used in your own custom research surveys, reach out for a demo.

Methodology

Morning Consult developed the above shopping profiles using a cluster analysis, specifically a partitioning around medoids method, also known as k-medoids, as the method to develop the clusters in this memo. This method of cluster analysis is robust, with an ability to include outliers and allow users to input exclusively quantitative or mixed features. The PAM analysis develops clusters by placing respondents into relatively homogenous groups based on distances between responses to the selected features. The features were selected for the cluster analysis with the intent to sort respondents based on what they value in brands and how they approach shopping, as well as how they view companies’ role in societal issues. Throughout this memo, the results of a six-cluster PAM model with mixed feature inputs were used for analysis.