‘Buy Now, Pay Later’ Users Significantly More Likely to Overdraft Than Nonusers

Key Takeaways

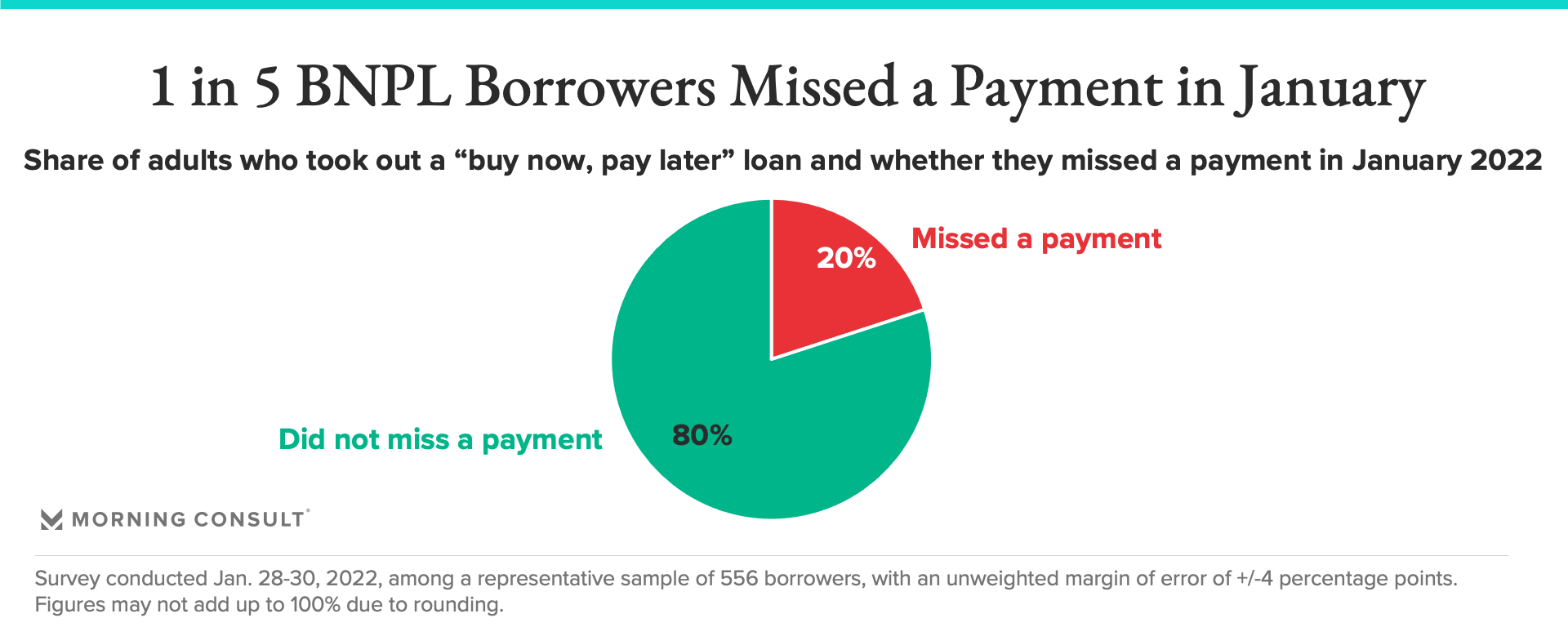

1 in 5 U.S. adults who took out a BNPL loan missed a payment in January, per a Jan. 28-30 Morning Consult survey.

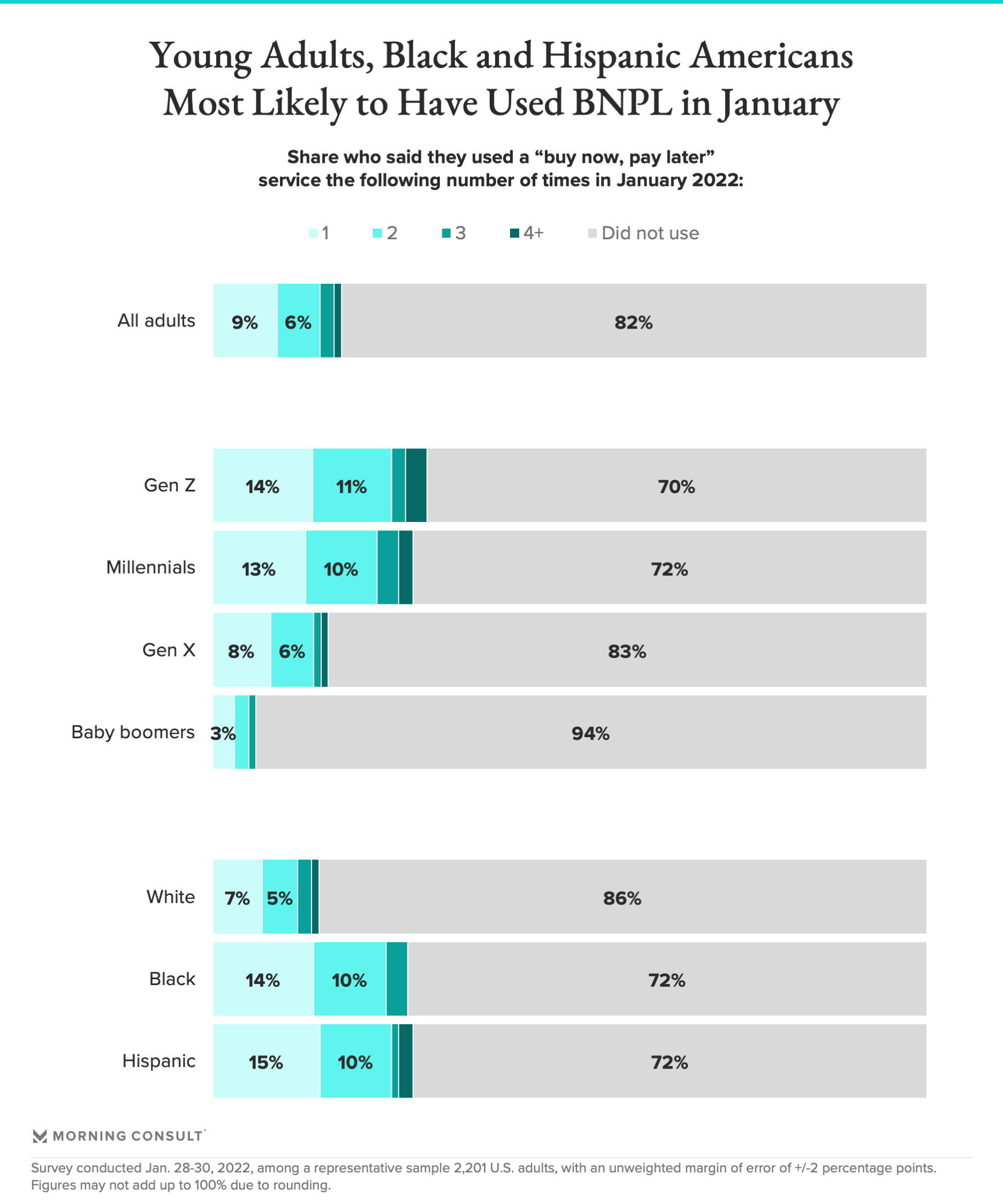

Gen Z, Black adults and Hispanic adults are more likely to use BNPL than the U.S. population as a whole.

Per the data and consumer advocates, it’s not clear that there’s causation between overdrafting and BNPL users.

Whether it’s purchasing a Peloton, a mattress or even booking a vacation, the rise of the “buy now, pay later” sector has made it easier and quicker to commit to large purchases online, often with the click of a few buttons. BNPL has drawn the attention of major fintechs and secured large sums of venture capital funding, but consumer advocates have warned of the potential for customers to overdraft their accounts, drawing increasing scrutiny from U.S. regulators.

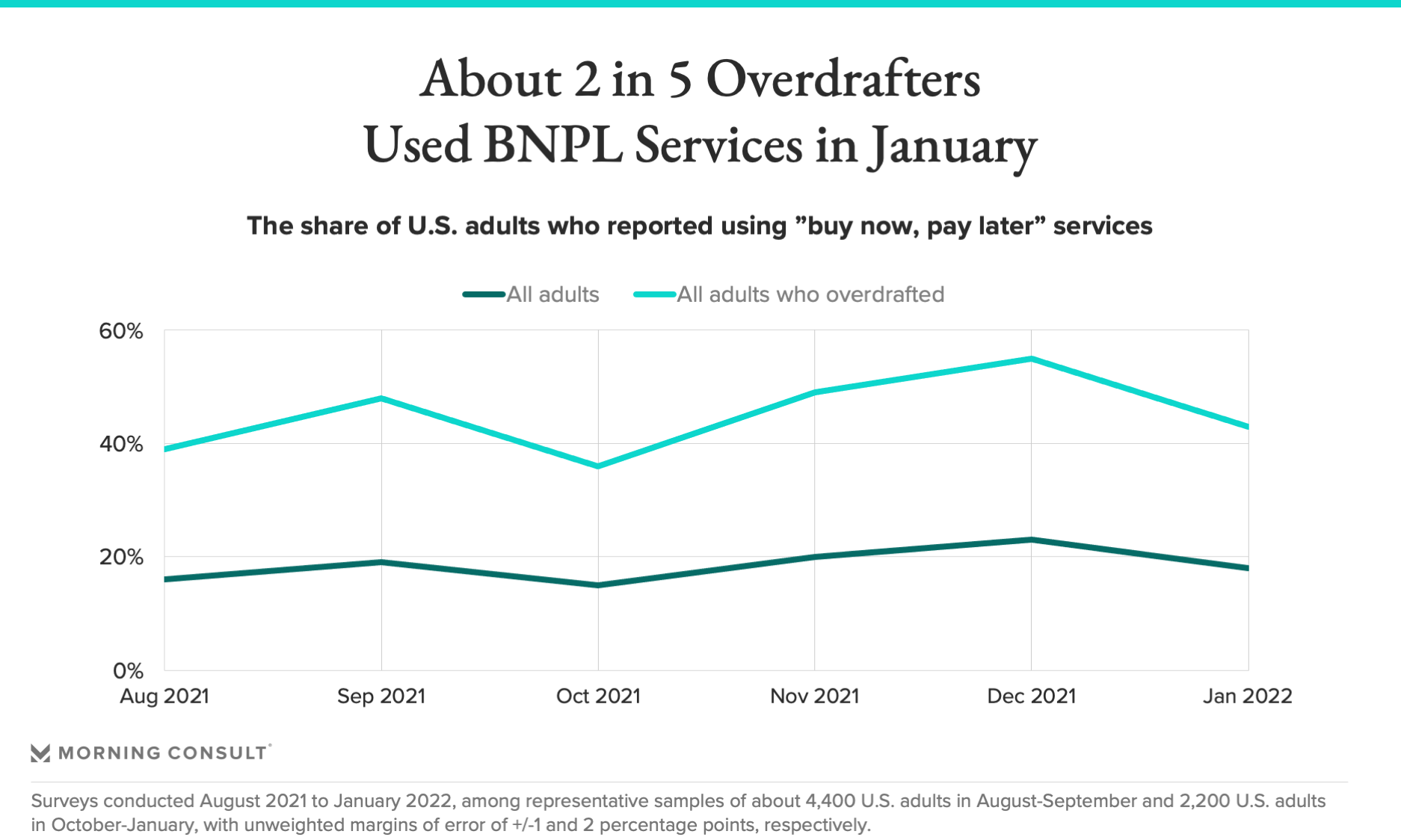

There is, in fact, substantial overlap between people who receive overdraft fees and those who use “buy now, pay later” products, according to an analysis of Morning Consult data, based on a survey of 2,200 adults conducted Jan. 28-30.

And in January, overdrafters were more than twice as likely as U.S. adults overall to have been users of BNPL services.

While it’s not clear whether that relationship is causal or if the two groups are just pulling from the same pool of people, the correlation between overdrafters and BNPL users is statistically significant at a 95 percent confidence interval, according to a logistic regression analysis run by Morning Consult, even when controlling for racial, income, gender, community and generational demographics.

Consumer advocates said the relationship between BNPL users and overdrafters is concerning. Lauren Saunders, associate director at the National Consumer Law Center who’s also testified in Congress about the BNPL sector, called the data “distressing but not surprising.”

“People who don’t have the money to pay for something in full today and people who are overdrafting are attracted to ‘buy now, pay later’ because it looks like a more affordable form of credit than it is,” she said.

The Financial Technology Association, a trade group that represents many BNPL firms, disputed the findings of Morning Consult’s analysis, saying that the data is misleadingly “equating BNPL with a pervasive problem.”

“When used responsibly, ‘buy now, pay later’ is an alternative to traditional high-cost credit, which often comes with double-digit APRs and costly fees,” said Penny Lee, chief executive of the trade group who’s testified in front of the House Financial Services Committee’s task force on financial technology about the benefits and risks of the sector.

In the survey question, Morning Consult defined BNPL as “a short term lending option that allows customers to make purchases at retailers without having to pay the entire amount up front,” and gave Afterpay, Klarna, Sezzle, QuadPay (now known as Zip) and Affirm as examples; the last one is not a Financial Technology Association member.

A trade group official said that its BNPL member companies “perform soft credit checks to assess the likelihood of repayment” and do not grant “access to their product if there are insufficient funds and shut off access when there is a failure to pay.”

The official also noted that most customers of its member companies use debit cards and that customers can avoid overdraft fees if they don’t opt into overdraft protection services. And several of the trade group’s member companies do not permit Automated Clearing House Network capabilities, the service that electronically transfers funds between banks via direct deposit, direct pay or electronic checks, which the official said is “another deterrent against overdraft.”

With usage peaking in December, “buy now, pay later” comes under regulatory scrutiny

Since BNPL boomed amid the COVID-19 pandemic – as consumers retreated into their homes and started shopping increasingly online – the Consumer Financial Protection Bureau has started looking critically at the sector.

Federal regulators are keeping an especially close watch on the BNPL sector around the holiday shopping season, as customers financed gifts increasingly with alternative payment methods and short-term loans. BNPL use peaked in December, with 23 percent of all U.S. adults saying they used the service, according to monthly surveys dating back to August 2021.

CFPB Director Rohit Chopra signaled increased scrutiny of the sector during a Washington Post Live event earlier this month, when he predicted that the most recent holiday season would “shatter records in terms of buy now, pay later adoption.”

“Part of what we need to do is make sure that we are monitoring these markets because we saw time and time again – and the American public has seen this over and over again – of law enforcement agencies and regulators simply just asleep at the switch, not understanding how markets work, and then being too late when things go badly wrong,” he said.

The relationship between overdraft and BNPL is a central part of some of the CFPB’s concerns about the sector. The agency has warned that the loans can cause overdraft fees if customers don’t have enough money in their accounts to service the payments. (The CFPB declined to comment for this story).

Bryan Schneider, formerly an associate director for supervision, enforcement and fair lending at the CFPB from 2019 to 2021, said that the relationship between overdraft and BNPL usage is something “regulators should be thinking about,” although he said people shouldn’t assume that BNPL “must be a bad product” because of the correlation.

“That would be entirely too narrow of a focus of a consumer’s financial life,” said Schneider, now a partner at the law firm Manatt, Phelps & Phillips in Chicago.

Another concern of consumer advocates and the CFPB is missed payments and the fees that can accumulate if customers do so frequently, further exacerbating the overdraft problem. Unlike more traditional short-term credit, such as making a purchase with a credit card, BNPL companies don’t perform an “ability to pay” analysis as required by the Truth in Lending Act, which some consumer advocates say makes them more likely to lend to people who can’t afford their loans.

According to Morning Consult’s survey, 20 percent of BNPL users missed a payment in January.

Young adults, minorities are more likely than other demographics to use BNPL

Because BNPL is sometimes used as an alternative to traditional credit cards, customers can find themselves in situations where they’re paying automatically out of one debit account for multiple retail purchases, which can get out of control and result in overdraft fees, said Taylor Roberson, federal policy counsel at the Center for Responsible Lending.

“When you have consumers who are using this as an alternative to credit, the customers are making the bank account the primary resource to pay back loans,” she said. “When there’s potentially issues of numerous loans from numerous companies, that’s the sort of situation where the likelihood of overdrafts goes way up.”

While a look at the data shows that overdrafters are significantly more likely to use BNPL than U.S. adults as a whole, it’s not clear if such loans are causing those overdrafts, Roberson and other consumer advocates cautioned.

BNPL product users tend to be younger people and minorities, according to Morning Consult data — the same groups most likely to overdraft.

The higher share of minorities and young people using BNPL is still something the CFPB will consider as it weighs oversight, said Michael Taiano, a senior director at Fitch Ratings who’s written about the BNPL sector and its regulatory outlook.

“If I was a regulator, I would be concerned that certain demographics are being taken advantage of in some shape or form,” he said.

Morning Consult data scientist Chris Cyr contributed.

Correction: A previous version of this story incorrectly stated that QuadPay is not a member of the Financial Technology Association; the BNPL platform, now known as Zip, is indeed a member.

Claire Williams previously worked at Morning Consult as a reporter covering finances.