The bottom line up front

Domestic beer is a category where the biggest brands are also the broadest—and that breadth is the real competitive moat. Bud Light leads in Mental Availability (i.e. the propensity of the brand to come to mind) not because it dominates any single drinking occasion, but because it shows up across nearly all of them: parties, sports, holidays, routine weeknight wind-downs. Miller Lite, its closest light-beer rival, trails by nearly 5 points in mental market share and is narrower in every demographic cut except one—the Midwest, where it closes the gap. The strategic question for beer brand challengers isn’t how to out-position Bud Light on a single occasion. It’s how to show up in more of them. Meanwhile, price sensitivity is the category’s dominant conversion barrier, and the brands that make the cost of choosing them feel predictable and painless will disproportionately benefit.

Cross-Category Context: Our companion U.S. Alcoholic Beverages Category Advantage study places domestic beer at ~14% mental market share across all beverage types—a lead of just 1 point over wine (~13%) and 4 points over imported beer (~10%). The breadth advantage that separates Bud Light from Miller Lite within domestic beer is the same structural advantage domestic beer as a category must defend against wine, spirits, and emerging alternatives. Domestic beer’s mental position among men shows a –2.6pp gap between share of mind and share of throat—meaning it is consumed more out of habit than active choice, making it vulnerable to any competitor that builds stronger occasion associations.

The Domestic Beer Category Today

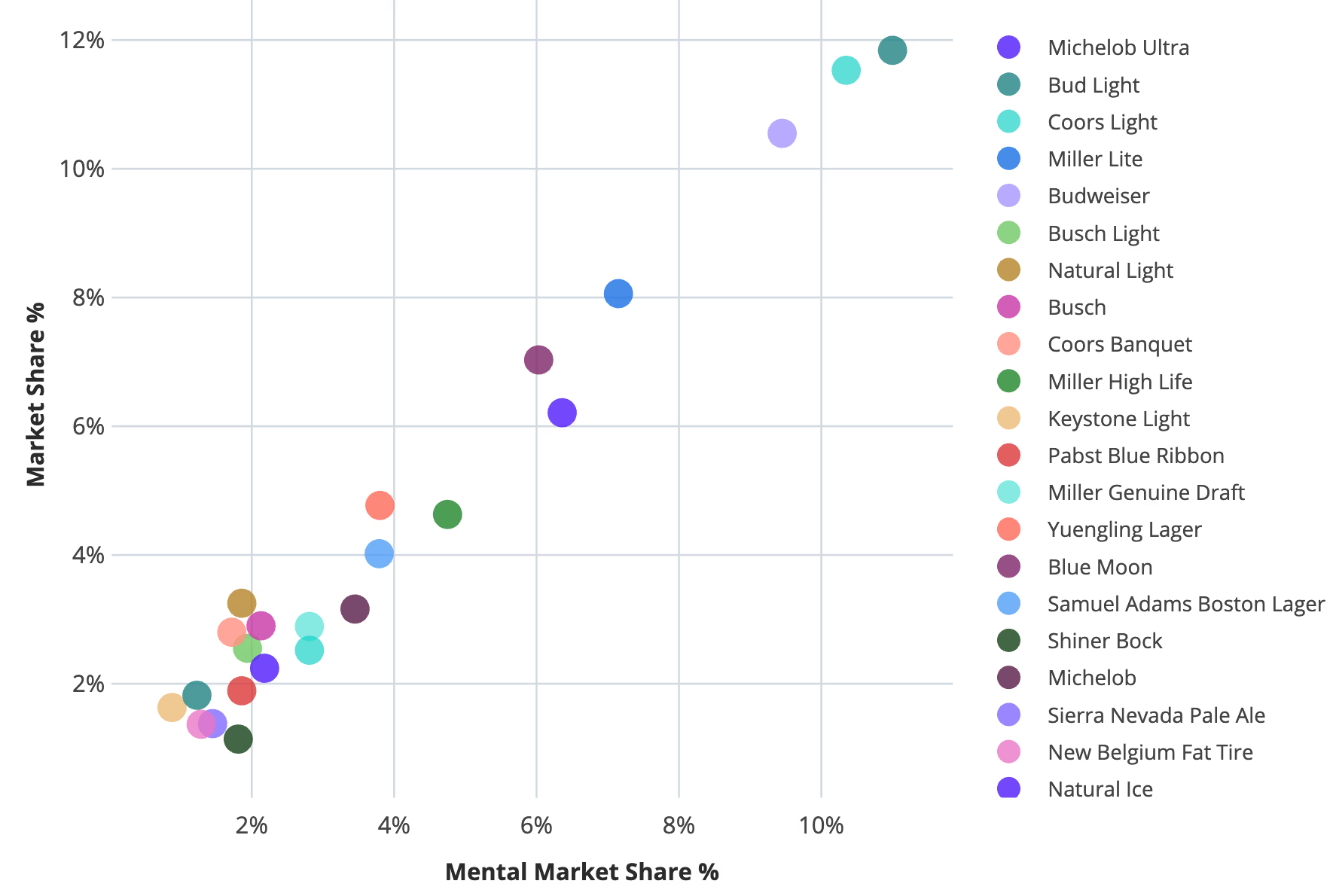

Bud Light is the category’s front door, but no brand dominates. With ~12% mental market share (the share of all brand-occasion associations in the category), Bud Light leads Budweiser (~10%), Coors Light (~9%), and Miller Lite (~7%). These four brands form a clear first tier. But even Bud Light’s lead is modest—this is a fragmented category where no single brand commands more than one in eight mental associations. Blue Moon (~6%) and Michelob Ultra (~6%) form a second tier with meaningfully different profiles: Blue Moon over-indexes among women, higher-income drinkers, and in the West; Michelob Ultra skews older and Southern.

Breadth of recall, not depth of loyalty, is the differentiator. Bud Light and Coors Light lead on network size—the number of distinct occasions a brand comes to mind—at roughly 8 occasions each, with Michelob Ultra and Budweiser close behind. Miller Lite trails at ~7.3. The brands with the widest recall networks are the ones surfacing for weeknight relaxation, gameday gatherings, holiday celebrations, and casual dinners alike. They don’t depend on one trigger firing.

Budweiser has more physical presence than its mental position suggests. Budweiser matches or exceeds Bud Light on awareness (~70% vs ~72%) and recent consumption (~22% each in the past four weeks), yet trails Bud Light by 2 points on mental market share. This gap between physical availability and mental availability is an opportunity signal—Budweiser is bought out of habit and access, but isn’t being thought of as broadly across purchase occasions.

Emotional connection is lukewarm across the board. On a 1–7 scale, the highest-scoring brand is Budweiser at 3.5, followed by Bud Light at 3.4 and Miller Lite at 3.3. No brand has built deep emotional resonance with the domestic beer consumer. The category is functionally driven—occasion and convenience, not identity and aspiration.

Cross-Category Context: Lukewarm emotional connection is not just a domestic beer characteristic—it is a competitive exposure point. Wine scores 3.9 on the same 7-point emotional connection scale with a more gender-balanced profile, and whiskey sustains strong emotional resonance through a narrow premium position. Categories that build emotional equity can defend occasions more durably than categories that compete on function alone.

Who Are Domestic Beer Consumers?

This is a younger-skewing, male-heavy, value-conscious audience most prominent in the South and Midwest. Higher-income drinkers ($100K+) are present but behave differently—they’re more likely to reach for Coors Light and Blue Moon, more triggered by dinner occasions and hosting, and less price-sensitive. The youngest cohort (21–34) is the most mentally open: they associate more brands with more occasions, but their associations are also the most volatile and least entrenched. This is the formation window.

Cross-Category Context: The gender skew is sharper than it appears in isolation. Across all alcoholic beverages, domestic beer’s MMS is 18.8% among men but only 11.6% among women—a –7.2pp gap that makes it one of the most male-skewed categories in the alcohol space. Wine runs +9.1pp female. Domestic beer’s female consumer base isn’t just “smaller”—it is structurally ceded to wine and vodka, and growth strategies that ignore cross-category gender dynamics are working with incomplete information.

The Moments That Matter

Domestic beer consumption triggers are social, routine, and overwhelmingly casual. The occasions that matter most cluster around two themes: relaxation and socializing.

“Relaxing at home after a long day” (~33%) — the single largest entry point. This is the category’s default occasion, and it doesn’t reward any one brand disproportionately. Bud Light, Budweiser, and Coors Light are tightly bunched at ~24–25%. The winner here isn’t the brand with the strongest home positioning—it’s the one already in the fridge.

“Socializing with friends on a night out” (~32%) and “Having drinks at a party or social gathering” (~30%) — the social cluster. Bud Light holds a slight edge across both, but the gap is narrow. These occasions reward ubiquity and group acceptability—the brand everyone can agree on.

“Watching sports or a big game” (~29%) — the most skewed occasion in the category. It over-indexes massively among Midwest drinkers (+11pp), high-income consumers (+10pp), and men (+6pp), while under-indexing among women (–8pp) and younger drinkers (–7pp). Budweiser and Bud Light lead here, but not by much.

Secondary triggers include hosting at home (~27%), casual/laid-back settings (~25%), and live events (~23%). Dinner occasions (~22%) and holiday celebrations (~21%) round out the middle tier.

Cross-Category Context: The at-home relaxation occasion is the most contested battleground across all alcoholic beverages. At the total-category level, domestic beer (43% association) and wine (41%) are virtually tied, while RTD cocktails (24%) and THC beverages (22%) are making inroads. The competitive threat to any domestic beer brand in this moment is not just another domestic beer—it is a glass of wine, a seltzer, or a THC beverage. And the at-home occasion splits sharply by gender: wine’s mental advantage for “relaxing at home” is +11.9pp for women but –2.8pp for men, meaning gender-aware messaging is essential for any brand trying to defend or grow this occasion.

How Segments Differ

The core structure holds, but three dimensions shift the weighting meaningfully:

Income: High-income drinkers ($100K+) are a different animal. They over-index on dinner occasions (+8pp), hosting (+9pp), and watching sports (+10pp). They pull toward Coors Light (+4pp MMS vs Total) and Blue Moon (+1.5pp), and away from Bud Light (–2.5pp). They also cite “limited variety” as a barrier at higher rates—they want range, not just availability. Lower-income consumers are more price-triggered and less occasion-diverse.

Age: Younger drinkers (21–34) show the highest mental penetration across almost every brand—they’re open, forming associations, and responsive to new signals. But they also show the widest gap between mental availability and actual consumption: they think of many brands but buy fewer of them. The conversion friction here is price and accessibility, not awareness. Older drinkers (65+) have sharply narrower recall networks and lower mental penetration; their choices are locked in.

Region: The Midwest is Miller Lite’s stronghold—MMS rises to ~11%, nearly matching Bud Light. Sports and party occasions over-index heavily. The South is Bud Light’s best region at ~14% MMS. The West is Blue Moon and Coors Light territory. The Northeast underperforms on network size for most brands, suggesting either less occasion diversity or fewer consumption contexts overall.

What's Blocking Conversion

Price and affordability friction is the dominant barrier. ~28% cite cost as a reason they’ve been prevented from consuming a specific domestic beer. This is universal but hits hardest among men (~31%) and older consumers (~30%). In a category where brands compete on near-identical price points, the perception of value—not the sticker price—is what separates consideration from purchase.

Availability and access friction is the second cluster. ~18% say their preferred brand isn’t available where they shop, and ~15% say it isn’t sold in the environments they’re in. This is a distribution and merchandising problem, not a marketing problem—and it’s more pronounced among lower-income consumers who shop in fewer retail channels.

Choice overload and convenience friction rounds out the picture. ~12% cite difficulty choosing in-store, and ~12% say smaller/convenient formats aren’t available. Younger drinkers (21–34) are the most affected by in-store confusion (~15%)—the paradox of high mental openness meeting a cluttered retail shelf.

Cross-Category Context: Price friction is even more pronounced at the total alcohol category level (~35%), and skews older (40% of 65+ vs 25% of 21–34). But the barrier that matters most for domestic beer’s cross-category position is complexity friction: 18% of 21–34-year-olds across all alcohol types say it’s “harder to choose in-store.” Beer’s format proliferation (variety packs, flavored extensions, hard seltzers sharing shelf space) contributes to the same confusion that historically favored beer’s simplicity advantage over spirits. Meanwhile, spirits face a preparation barrier (16%) that RTD cocktails solve structurally—a growing threat to beer’s convenience positioning.

Why This Matters Now

“Breadth beats depth” is the structural law of this category. The brands with the widest recall networks—showing up for relaxation, sports, parties, dinners, and holidays—are the brands with the highest mental market share. Investing in one occasion (even sports, even parties) caps growth. Investing in being thought of across many occasions compounds it.

Miller Lite’s path isn’t about matching Bud Light nationally—it’s about exploiting its regional advantage and closing the breadth gap. Miller Lite’s Midwest MMS (~11%) nearly matches Bud Light, but it collapses in the South (~7% vs ~14%) and the West (~5% vs ~9%). Expanding occasion associations outside of the Midwest—particularly in social and hosting contexts where it already has latent presence—is the highest-leverage play.

Price sensitivity demands clarity, not discounting. When cost is the top barrier at ~28%, the brands that win aren’t necessarily the cheapest—they’re the ones where the value proposition is most obvious and predictable. Bundle messaging, pack-size transparency, and visible everyday pricing will outperform promotional discounting.

Young drinkers are open—and confused. The 21–34 cohort shows the highest mental penetration for almost every brand, but also the highest rates of in-store choice confusion and the widest gap between consideration and purchase. Simplifying the path from “I’ve heard of it” to “I’m grabbing it”—through packaging, shelf placement, and format availability—is the growth lever for this generation.

The category itself must defend its position, not just the brands within it. Everything in this memo describes the competition among domestic beer brands. But the total alcoholic beverages landscape shows that domestic beer’s mental position is being pressured from above—wine and spirits taking elevated and emotional occasions—and from below—RTD cocktails, hard seltzer, THC beverages, and non-alcoholic options capturing health-conscious and convenience-driven moments. The GLP-1 effect compounds this: over a quarter of alcohol consumers now have a medicalized reason to reconsider consumption, and the “better for you” shelf is splitting into non-alcoholic beverages for women and THC beverages for men. The “breadth beats depth” thesis holds within domestic beer, but the category as a whole needs to defend its breadth position against substitutes, not just internal rivals

About this research

Morning Consult conducts over 30,000 daily proprietary surveys in 45 countries covering more than 5,000 brands and 50 economic indicators.

Our category advantage research is aimed at understanding the needs driving consumers in your category — and how your brand can own more of them. This research is built on validated principles of brand-driven growth and powered by Morning Consult’s industry-leading sampling technology.

Measure the true drivers of brand strength

Capture both mental availability (the likelihood your brand comes to mind when consumers face a need or occasion) and emotional closeness (how strongly consumers connect with your brand), benchmarked against competitors.

Uncover Category Entry Points (CEPs)

Directly tied to mental availability, see the specific needs, occasions, and triggers that drive purchase decisions in your category, and how strongly your brand is linked to them.

Pinpoint growth opportunities

Direct investment toward the moments and consumer segments with the greatest potential to grow your brand.

Turn insights into action fast

Get survey results in 4–5 days through a centralized dashboard and short-form memo that equips stakeholders with clear direction on where and how to win.

Learn more

YouTube TV Brand Strength: Live Sports, News & Streaming vs. Netflix, Hulu, Amazon Prime

.png)

Why LinkedIn Is the Social Media Category's Specialist

.png)