The bottom line up front

American Express' Platinum Card leads the premium credit card category on every core mental availability metric — Mental Market Share (~24.5%), Mental Penetration (~80.5%), and recall breadth — but it leads a category whose central purchase trigger it is structurally disadvantaged on. The #1 reason consumers reach for a premium card is maximizing cashback and points across spending categories (~33% salience), and Amex under-indexes on that occasion more than almost any other brand (−6.3). The brand owns the travel and lifestyle corridor with conviction — but the category's front door opens on a trigger American Express is not answering. The strategic imperative is not to abandon the travel identity, but to extend mental availability into the optimization occasions before Chase or Capital One consolidates them.

Where American Express Stands in the Premium Credit Card Category

The brand leads the category — but the lead is built on a narrower occasion footprint than awareness numbers suggest. At ~24.5% Mental Market Share, Amex sits meaningfully ahead of Chase (~20.4%) and Capital One (~19.9%), with an 80.5% mental penetration that is the highest in the category. On raw recall, no brand comes close. The challenge is that the Network Size (9.75) — the average number of occasions the brand is linked to — is only marginally ahead of Chase (9.53) and Capital One (9.49). American Express is thought of by more people, but not for meaningfully more reasons. That gap between penetration leadership and network parity is the signature of a brand that has earned broad awareness but not yet converted it into occasion versatility.

American Express is thought of widely, but not felt deeply. On a 1–7 emotional connection scale, Amex scores 3.2 — not the lowest in the category, but well below what the brand's heritage and annual fee premium would predict. Capital One, a brand a third of Amex's age, matches it. This isn't a crisis, but it is a strategic vulnerability: in a category where annual fees run for at least hundreds of dollars and renewal decisions are annual, emotional resonance is not aesthetic — it is retention. Consumers who can calculate their card's value but don't feel connected to the brand are one better offer away from switching.

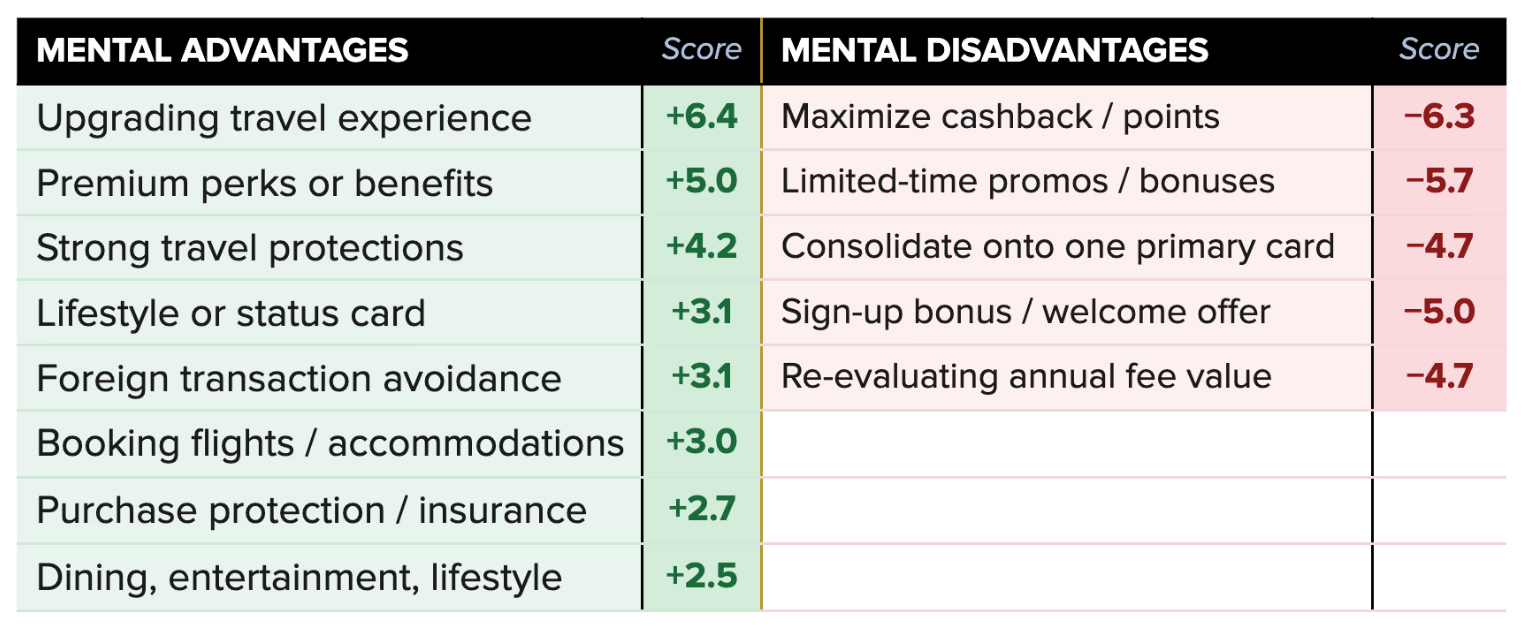

The mental advantage data reveals a clear, defensible travel corridor — and a meaningful disadvantage in the occasions that drive the most category volume. Amex holds its strongest advantages on upgrading travel experiences (+6.4), premium perks (+5.0), strong travel protections (+4.2), and foreign transaction avoidance (+3.1) — a coherent and well-earned cluster. But it under-indexes significantly on the category's single highest-salience trigger, maximizing cashback and points (−6.3), as well as on promotional bonuses (−5.7), consolidating spending onto one primary card (−4.7), and sign-up bonus offers (−5.0). These are the occasions that fire most frequently, and Amex is disadvantaged on all of them.

The CEPs American Express Owns — and the Ones It Doesn’t

The travel and access cluster is Amex's genuine competitive moat. No other brand comes close on upgrading travel experiences (+6.4, category-leading by a wide margin), and Amex leads or co-leads on booking flights and accommodations (+3.0), premium perks and benefits (+5.0), and foreign transaction fee avoidance (+3.1). The lifestyle and status CEP (+3.1) adds a second cluster — dining and entertainment (+2.5) rounds out a brand that has coherently built mental availability around affluent, experience-oriented spending. These positions are earned and should be defended, not diluted.

The optimization cluster — where the category's volume lives — is Amex's structural blind spot. The #1 purchase trigger in the category, maximizing cashback and points across spending categories (~33% salience), is the CEP on which Amex has its single largest disadvantage (−6.3). Chase and Capital One benefit here; U.S. Bank and Bilt over-index. The sign-up bonus occasion (~20% salience), the promotional transfer bonus occasion (~23% salience), and the annual fee re-evaluation occasion (~15% salience) all show similar Amex deficits. Together, these occasions represent a substantial share of the category's consideration events — and the brand is functionally absent from the mental conversation when they fire.

The "consolidate onto one primary card" occasion is a missed strategic bridge. At ~15% salience, consolidating spending onto one primary card is exactly the occasion where a premium card with broad acceptance and strong rewards should win — and Amex under-indexes (−4.7) while Chase (+4.5) and Bank of America (+4.7) lead. This is a direct consequence of the lingering acceptance perception gap: ~13% of respondents cite Amex's not being accepted everywhere as a barrier. Where that perception persists, consolidation consideration collapses.

Who American Express Is Winning — And Losing

Amex is the dominant brand among older, higher-education consumers — and that is a double-edged position. MMS climbs from ~21% among 18–34 year olds to ~32% among 65+ consumers, with a similar step-up at 45–64 (~29%). Among post-grad consumers, Amex holds ~27% MMS. This is valuable: older, more educated consumers carry premium cards at higher rates and generate more annual fee revenue. But building the brand's strongest mental availability in an aging cohort — while the 18–34 cohort shows only marginal Amex advantage over Chase and Capital One — creates a structural succession problem.

Among younger consumers, the category is genuinely contested and Amex has no structural advantage. Among 18–34 year olds, Amex MMS (~21.3%) leads Chase (~19.5%) and Capital One (~15.9%) — but by a margin that reflects general brand awareness rather than earned occasion relevance. This is the cohort most responsive to sign-up bonuses, promotional offers, and cashback optimization — precisely the occasions on which Amex is disadvantaged. If the 18–34 cohort forms its primary card association around Chase or Capital One during the next three years, Amex's MMS aging curve accelerates.

The female segment is Amex's most underleveraged asset. Amex's female MMS (~27.5%) is ~6 points higher than male (~21.7%) — a gap that doesn't appear for any competitor. The brand carries meaningfully stronger resonance among women, almost certainly anchored in its access, service, and premium-experience associations. Female premium card consumers over-index on the dining, lifestyle, and access occasions that are Amex's strongest CEPs — and there is no evidence the brand's messaging treats this alignment as a targeting priority.

Geography is stable — Amex has no regional weakness to fix. Unlike Capital One (Midwest-heavy) or Chase (slight West underperformance), Amex holds consistent MMS across all four regions within a 2-point band (~23–26%). This is the mark of a genuinely national front-door brand and an asset to protect, not a dynamic that requires intervention.

What's In the Way

The brand's conversion problem is specific and diagnosable: fee legibility, not awareness. Aided awareness at ~73% is the highest in the category. MMS at ~24.5% is the highest in the category. The bottleneck is between consideration and purchase. The annual fee is cited as a barrier by ~40% of total respondents — and this rises sharply among the 45–64 cohort (~47%) and 65+ (~54%), which are exactly the segments where Amex's mental availability is strongest. The brand is building recall in segments where fee anxiety is highest. More awareness advertising will not solve this.

The acceptance perception gap is a specific, closeable drag. The "not accepted everywhere" barrier (~13%) is disproportionately an Amex problem — and unlike fee friction, it is based on a perception gap rather than a product reality. Amex's acceptance footprint has expanded substantially, but the mental association with limited acceptance persists. This suppresses conversion on the "consolidate onto one primary card" occasion directly and creates hesitation in everyday spending occasions where Amex wants broader mental availability.

Rewards complexity compounds the optimization disadvantage. With ~37% of respondents citing some form of rewards complexity as a barrier, the category's UX problem hits Amex particularly hard because its value proposition is the most complex to calculate. Membership Rewards points, transfer partners, statement credits, and tiered benefits are genuinely valuable — but require effort to extract. For a brand already disadvantaged on the "maximize my cashback" occasion, complexity friction is a second-order barrier that further suppresses conversion in the optimization moments.

About this research

Morning Consult conducts over 30,000 daily proprietary surveys in 45 countries covering more than 5,000 brands and 50 economic indicators.

Our category advantage research is aimed at understanding the needs driving consumers in your category — and how your brand can own more of them. This research is built on validated principles of brand-driven growth and powered by Morning Consult’s industry-leading sampling technology.

Measure the true drivers of brand strength

Capture both mental availability (the likelihood your brand comes to mind when consumers face a need or occasion) and emotional closeness (how strongly consumers connect with your brand), benchmarked against competitors.

Uncover Category Entry Points (CEPs)

Directly tied to mental availability, see the specific needs, occasions, and triggers that drive purchase decisions in your category, and how strongly your brand is linked to them.

Pinpoint growth opportunities

Direct investment toward the moments and consumer segments with the greatest potential to grow your brand.

Turn insights into action fast

Get survey results in 4–5 days through a centralized dashboard and short-form memo that equips stakeholders with clear direction on where and how to win.

Learn more

.png)

Why the Bank of America Premium Rewards Elite Card Faces an Under-Recall Challenge

-1.png)

ChatGPT Leads the Consumer AI Category on Every Core Mental Availability Metric

.png)