The bottom line up front

The Bank of America Premium Rewards Elite card has the category's clearest under-recall problem: 52% aided awareness but only 11.5% Mental Market Share — a gap that means millions of consumers who know the brand don't reach for it when premium card decisions arise. The mental advantage data points to a brand with real strengths in consolidation, foreign transaction avoidance, and expense management — functional, trust-based occasions that align naturally with Bank of America's broader relationship banking identity. The strategic opportunity is not repositioning; it is converting an existing relationship advantage (banking customers who already trust the brand) into premium card mental availability through occasions the brand is already credibly positioned on.

Where the Bank of America Premium Rewards Elite Card Stands in the Premium Credit Card Category

Bank of America is the category's clearest case of awareness outrunning mental availability. At 52% aided awareness — fourth-highest in the category — and just 11.5% Mental Market Share, Bank of America demonstrates the classic under-recall gap: a brand widely recognized but rarely top-of-mind when premium card consideration fires. Its Mental Penetration (66.6%) confirms that two-thirds of category-aware consumers do link the brand to at least one occasion. The problem is depth: Network Size (8.65) trails the top three brands by 1–1.1 points, meaning consumers who think of BofA link it to fewer situations than they link to competitors.

The emotional connection signal is average — which is a problem when the brand needs to justify under-recall. At ~3.43 on a 1–7 scale, Bank of America's mean emotional connection score actually leads American Express and Chase. But this warmth isn't converting into premium card mental availability — suggesting the affective connection is with Bank of America as a banking institution, not specifically with its premium card product. Unlocking this emotional asset for card acquisition requires building a distinct premium card identity that sits on top of, rather than blending into, the broader banking brand.

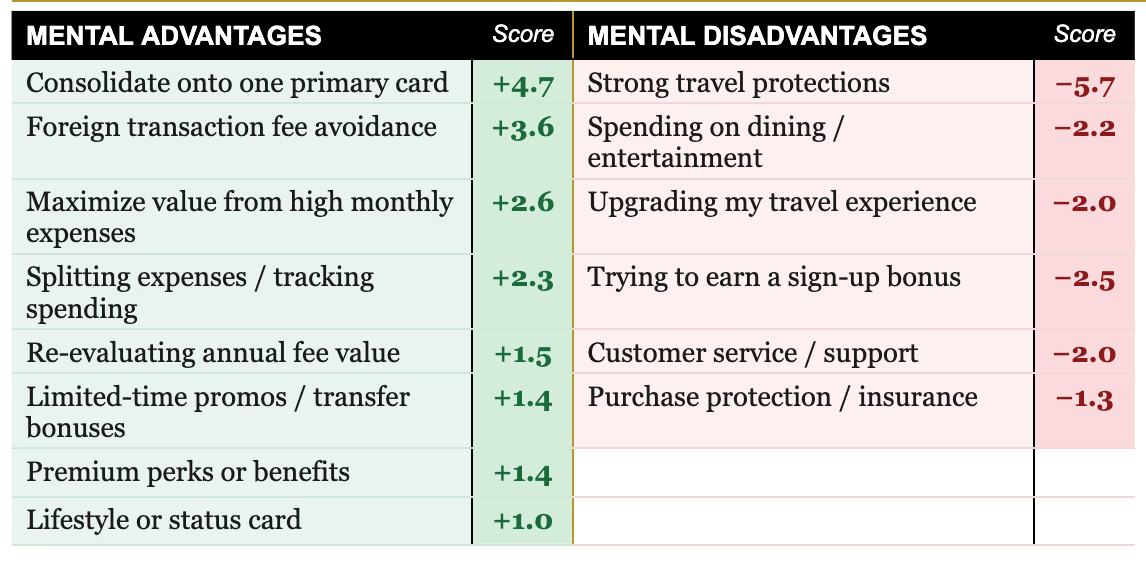

The mental advantage profile is coherent and actionable — a functional trust brand in a category that skews experiential. Bank of America over-indexes on consolidation (+4.7), foreign transaction avoidance (+3.6), high-spend value maximization (+2.6), and expense tracking (+2.3). These are everyday financial utility occasions — exactly the occasions a banking customer would naturally associate with their primary bank's card. The disadvantages cluster around travel premium (strong travel protections −5.7, travel experience upgrading −2.0) and dining (-2.2). This is not a confused brand; it is a functionally coherent brand with an aspirational gap.

The CEPs Bank of America Owns — and the Ones It Doesn’t

Consolidation is Bank of America's single strongest mental advantage — and a natural extension of banking relationships. At +4.7 on "consolidate onto one primary card," Bank of America leads or ties Chase for the top position on this occasion. For existing Bank of America banking customers, consolidating card spending with their primary bank is a natural behavior — and the Premium Rewards Elite card is positioned to be that consolidation vehicle. The brand's foreign transaction advantage (+3.6) adds an international travel dimension that extends the consolidation story beyond domestic utility.

The expense management cluster is under-communicated but strategically coherent. Bank of America's over-indexes on high-spend value (+2.6), expense tracking (+2.3), and annual fee re-evaluation (+1.5) form a consistent "financial control" narrative. This is not the most glamorous card positioning — but it is highly relevant to the ~$100K+ income consumers who most closely manage their financial picture and for whom a card that integrates with their banking relationship has genuine utility value.

Travel occasions are the structural gap that prevents premium positioning. The strong travel protections disadvantage (−5.7) is the steepest in the category for Bank of America — particularly notable given that travel protection is a core feature of most premium cards. Dining and entertainment (−2.2) and travel experience upgrading (−2.0) compound the picture: the brand is simply not associated with the experiential spending that premium card consumers aspire to. Until some travel occasion credibility is built, Premium Rewards Elite will remain mentally positioned below Amex, Chase, and Capital One on the premium card ladder.

Who Bank of America Is Winning — And Losing

The under-recall gap is the primary strategic problem — and it is not an awareness problem. With 52% aided awareness, the issue is not that consumers don't know Bank of America. The issue is that knowing Bank of America as a bank does not translate into reaching for the Premium Rewards Elite when a premium card occasion fires. Building a distinct premium card identity — with its own name recognition, benefits story, and mental availability — is the conversion lever.

Travel protections disadvantage (−5.7) undermines the premium card pitch. When consumers consider a $550/year card, travel protection is a core expected benefit. Bank of America's sharpest mental disadvantage on this occasion creates a credibility gap at the exact moment of premium card comparison. This is addressable through benefit communications — the product likely delivers travel protections — but the brand is not getting mental credit for them.

Fee complexity barriers hit a brand that hasn't built a clear value narrative. The ~40% fee barrier and ~37% rewards complexity barrier are category-wide — but they are particularly damaging for a brand whose primary awareness is as a utility banking institution rather than a premium card destination. Consumers who aren't sure what the card offers default to the brand they feel confident about: Amex or Chase.

What's In the Way

The under-recall gap is the primary strategic problem — and it is not an awareness problem. With 52% aided awareness, the issue is not that consumers don't know Bank of America. The issue is that knowing Bank of America as a bank does not translate into reaching for the Premium Rewards Elite when a premium card occasion fires. Building a distinct premium card identity — with its own name recognition, benefits story, and mental availability — is the conversion lever.

Travel protections disadvantage (−5.7) undermines the premium card pitch. When consumers consider a $550/year card, travel protection is a core expected benefit. Bank of America's sharpest mental disadvantage on this occasion creates a credibility gap at the exact moment of premium card comparison. This is addressable through benefit communications — the product likely delivers travel protections — but the brand is not getting mental credit for them.

Fee complexity barriers hit a brand that hasn't built a clear value narrative. The ~40% fee barrier and ~37% rewards complexity barrier are category-wide — but they are particularly damaging for a brand whose primary awareness is as a utility banking institution rather than a premium card destination. Consumers who aren't sure what the card offers default to the brand they feel confident about: Amex or Chase.

About this research

Morning Consult conducts over 30,000 daily proprietary surveys in 45 countries covering more than 5,000 brands and 50 economic indicators.

Our category advantage research is aimed at understanding the needs driving consumers in your category — and how your brand can own more of them. This research is built on validated principles of brand-driven growth and powered by Morning Consult’s industry-leading sampling technology.

Measure the true drivers of brand strength

Capture both mental availability (the likelihood your brand comes to mind when consumers face a need or occasion) and emotional closeness (how strongly consumers connect with your brand), benchmarked against competitors.

Uncover Category Entry Points (CEPs)

Directly tied to mental availability, see the specific needs, occasions, and triggers that drive purchase decisions in your category, and how strongly your brand is linked to them.

Pinpoint growth opportunities

Direct investment toward the moments and consumer segments with the greatest potential to grow your brand.

Turn insights into action fast

Get survey results in 4–5 days through a centralized dashboard and short-form memo that equips stakeholders with clear direction on where and how to win.

Learn more

How GLP-1 Reshapes Users’ Relationship to Casual Dining

.png)

Why American Express' Platinum Card Leads the Premium Credit Card Category

.png)