The bottom line up front

Chase Sapphire Reserve is the most consistently positioned brand in the premium credit card category — recalled by roughly the same share of consumers across every demographic cut, and mentally linked to more occasions per aware consumer than any other non-Amex brand. Its Mental Market Share (~20.4%) and broad optimization-trigger advantages make it the best-placed challenger to consolidate the category's highest-salience purchase occasion, maximizing value across spending. The strategic question for Chase is not how to grow awareness — it is how to convert consistent recall into emotional depth, and how to close the gap with American Express on the travel occasions that still drive premium card aspiration.

Where Chase Sapphire Reserve Stands in the Premium Credit Card Category

Chase is the category's most balanced brand — and that balance is both its strength and its ceiling. At ~20.4% Mental Market Share and 76.1% mental penetration, Chase sits just behind American Express and is statistically level with Capital One. Its Network Size (9.53) is nearly identical to Amex's (9.75), meaning Chase is linked to almost as many purchase occasions as the category leader. The brand's MMS is remarkably stable across gender, region, and education — no demographic cut moves it more than 3 points in either direction. This is the architecture of a front-door brand, but without the emotional premium that would justify taking share.

Chase is thought of consistently, but not felt distinctively. Its emotional connection score (~3.2 out of 7) matches American Express — the category's heritage leader — and leads Capital One (~3.4) only marginally when factoring sample variance. Chase has built broad, reliable recall without building a recognizable emotional identity. In a category where the top three brands are within 5 points of MMS parity, emotional differentiation is the available battleground — and Chase is not fighting it yet.

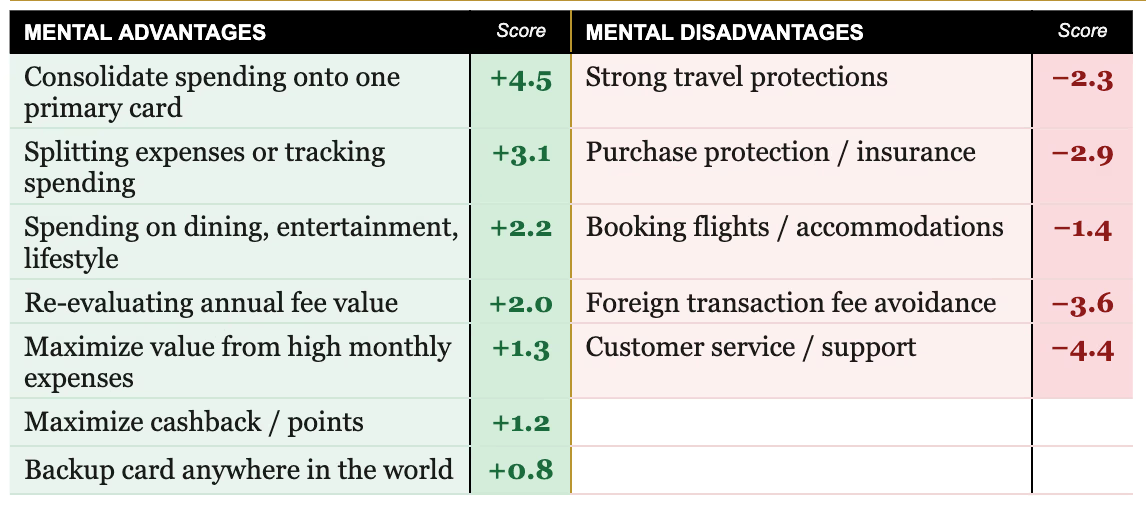

The mental advantage data reveals a brand built for everyday financial utility — not travel aspiration. Chase over-indexes meaningfully on consolidating onto one primary card (+4.5), splitting and tracking expenses (+3.1), dining and entertainment (+2.2), and re-evaluating annual fee value (+2.0). It holds modest but positive positions on cashback optimization and high-spend value maximization. The disadvantages are symmetric: Chase under-indexes on every travel-adjacent occasion — travel protections (−2.3), booking flights (−1.4), foreign transaction avoidance (−3.6). This is a brand that wins when consumers are thinking financially, and loses when they're thinking experientially.

The CEPs Chase Owns — and the Ones It Doesn’t

Consolidation and daily utility are Chase's genuine competitive advantages. The "consolidate onto one primary card" Category Entry Point (+4.5) is Chase's strongest position — and it leads the category on this occasion, ahead of Bank of America (+4.7) and well ahead of American Express (−4.7). Given that the category's acceptance barrier disproportionately affects Amex, Chase is the natural beneficiary when consumers want a single card for everything. The dining and entertainment over-index (+2.2) is a valuable secondary position that gives Chase an everyday-life anchor alongside its financial utility story.

The optimization occasions are Chase's growth opportunity. The category's #1 trigger — maximizing cashback and points — shows Chase with a modest but positive advantage (+1.2). This is not a strong position, but it is the right direction, and combined with the high-monthly-expense-value CEP (+1.3), it outlines a plausible path to owning the optimization cluster that no brand currently controls. The annual fee re-evaluation occasion (+2.0) is a natural bridge: consumers questioning their card value are exactly the audience Chase should be converting.

Travel occasions remain structurally weak — and ceding them entirely is a risk. Chase under-indexes on booking flights (−1.4), travel protections (−2.3), and foreign transaction avoidance (−3.6). For the Sapphire Reserve — a product with airport lounge access, travel insurance, and dining credits — this is a disconnect between product reality and mental availability. The card's travel benefits are not translating into travel occasion ownership. Amex dominates this space; Capital One is making inroads. Without some presence in travel CEPs, Chase risks being mentally positioned as the "sensible card" while competitors hold the aspirational occasions.

Who Chase Is Winning — And Losing

The 35–44 cohort is Chase's best segment — and it's contested. Chase's MMS peaks at ~23.4% among 35–44 year olds — its strongest demographic cut. This is also Capital One's best segment (~26.1%), making 35–44 the most competitive battleground in the category. This cohort is entering peak earning years and peak premium card usage; winning here has disproportionate long-term value. Chase's dining and consolidation advantages align well with 35–44 spending patterns — the question is whether its messaging is specific enough to win the segment rather than tie it.

Post-grad consumers are Chase's highest-education strength — and a direct Amex competitive window. Among post-grad consumers, Chase holds ~24.5% MMS — its strongest education segment, and only 2 points behind Amex (~26.8%). This is the segment most likely to carry $500+ annual fee cards and most likely to actively optimize their rewards. Chase's advantage on fee re-evaluation (+2.0) and daily tracking (+3.1) speaks directly to this audience's analytical mindset.

The West is Chase's relative weakness — and it matters. Chase's MMS in the West (~18.4%) is its lowest regional score, 2 points below its national average and notably below Amex (~23.4%) and Capital One (~17.7%). The West is the region where travel culture and card optimization intersect most intensely — exactly the occasion cluster Chase is disadvantaged on. A brand that can't hold its share in the region where premium card consumers are most engaged is leaving a disproportionately valuable audience on the table.

What's In the Way

Chase's primary conversion barrier is not awareness or recall — it's emotional inertness. With ~70% aided awareness and consistent MMS across demographics, Chase has no reach problem. The gap is between being thought of and being chosen — and in a category where emotional connection predicts renewal, Chase's flat 3.2 emotional score is a retention liability. Consumers who chose Chase for rational reasons (rewards structure, fee value) are more likely to churn when a competitor makes a better rational offer. Emotional resonance creates switching friction that data doesn't.

The fee complexity barrier hits Chase's strongest segments hardest. Rewards complexity (~37% of respondents) and annual fee justification (~40%) are the category's dominant friction clusters — and they are most acute among the post-grad and 35–44 cohorts that are Chase's best segments. Chase's positioning on fee re-evaluation (+2.0) creates an opening: consumers already reconsidering their card value are primed to switch to a brand that makes its value legible. Chase needs to be the answer to that reconsideration, not a bystander to it.

Customer service under-indexing (−4.4) is Chase's sharpest mental disadvantage — and a brand risk. The "wanting better customer service" CEP is Chase's steepest disadvantage across all occasions. In a category where cards are carrying $500–$695 annual fees, service expectations are premium. This is not a trivial gap — it will suppress conversion among the high-value consumers who most scrutinize what they're paying for.

About this research

Morning Consult conducts over 30,000 daily proprietary surveys in 45 countries covering more than 5,000 brands and 50 economic indicators.

Our category advantage research is aimed at understanding the needs driving consumers in your category — and how your brand can own more of them. This research is built on validated principles of brand-driven growth and powered by Morning Consult’s industry-leading sampling technology.

Measure the true drivers of brand strength

Capture both mental availability (the likelihood your brand comes to mind when consumers face a need or occasion) and emotional closeness (how strongly consumers connect with your brand), benchmarked against competitors.

Uncover Category Entry Points (CEPs)

Directly tied to mental availability, see the specific needs, occasions, and triggers that drive purchase decisions in your category, and how strongly your brand is linked to them.

Pinpoint growth opportunities

Direct investment toward the moments and consumer segments with the greatest potential to grow your brand.

Turn insights into action fast

Get survey results in 4–5 days through a centralized dashboard and short-form memo that equips stakeholders with clear direction on where and how to win.

Learn more

.png)

Why American Express' Platinum Card Leads the Premium Credit Card Category

How GLP-1 Reshapes Users’ Relationship to Casual Dining

.png)