The bottom line up front

The vodka category is mentally fragmented. No brand clears 20% Mental Market Share, and the top three — Smirnoff, Grey Goose, and Tito’s — each win different occasions with different consumers. That internal leaderboard matters less than an uncomfortable external reality: among women, vodka is one of the most autopilot-driven positions in alcohol. Women drink more vodka than they mentally associate with specific occasions (13.8% share vs. 10.0% mental share — a 3.8pp gap, the largest of any category in the alcohol landscape). That habit isn't anchored to strong occasion associations, which makes it the most exposed share position in the female alcohol market. Growth inside vodka will not come from more awareness. It will come from defending that position against categories — wine, RTDs, non-alcoholic — that are building stronger mental architecture among the next generation of drinkers.

Cross-Category Context: This memo covers vodka-specific dynamics. For cross-category context — including how vodka’s occasion share compares to beer, wine, tequila, RTD cocktails, and non-alcoholic options — see the companion Alcohol Category Advantage study. Where relevant, cross-category implications are flagged below.

The Vodka Category Today

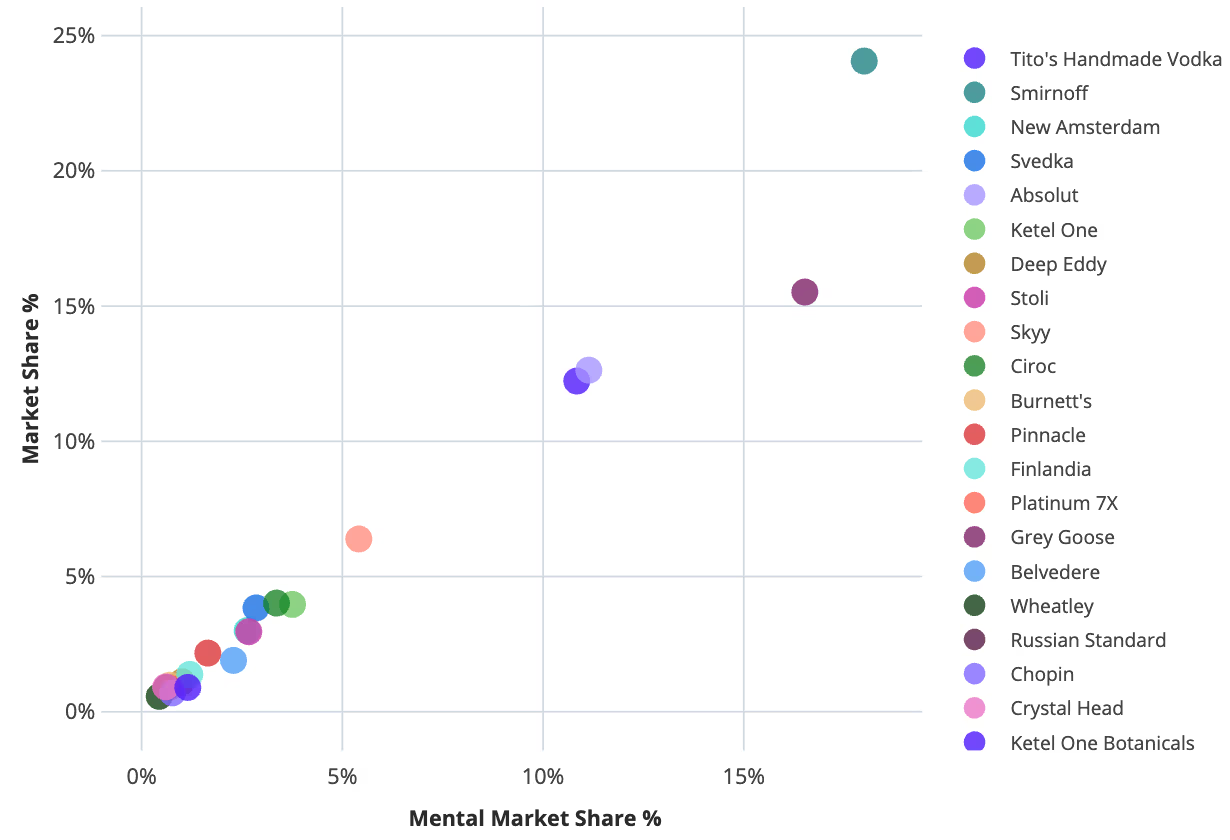

The leaderboard is crowded at the top and lonely below. Smirnoff (~18% MMS), Grey Goose (~16%), Tito’s (~11%), and Absolut (~9%) together account for roughly 55% of all mental associations inside vodka. Every other brand sits under 6%. A concentrated top with a long tail of brands that exist in the trade but barely exist in consumers’ heads.

Smirnoff is broadly available; Grey Goose owns clear white space. Smirnoff remains competitive across many high-salience occasions but rarely wins by a wide margin — it’s the broad, safe default. Grey Goose’s clearest white-space ownership is premium/refined (~45%) and smooth/easy (~43%): a narrower franchise, but a more defensible one.

Tito’s is the quiet contender. Third in MMS but matches or beats Grey Goose on most everyday occasions — hosting (~46%), holidays (~46%), reliable go-to for cocktails (~43%). It also has the widest overall network size in the category (10.6). Aided awareness only 46% versus Smirnoff’s 71%, meaning Tito’s over-converts on the awareness it has.

But these brands are fighting a two-front war. Inside vodka, they fight each other. Outside vodka, they fight an emerging tier — hard seltzer, RTD cocktails, THC beverages, and non-alcoholic options — that collectively holds under 12% of total alcohol MMS yet achieves 52–78% mental penetration among 21–34. These alternatives are the mental architecture of the next generation of drinkers. Planning against the legacy vodka leaderboard alone is solving last year’s game.

The Moments that Matter in the Vodka Category

Three occasions dominate vodka’s internal trigger landscape: socializing with friends (~33%), party or gathering (~31%), and relaxing at home (~27%). These default triggers reward breadth and ubiquity, which is why Smirnoff stays competitive across them.

A middle tier of hosting-and-holiday occasions (~20–23% salience each) rewards occasion-specific equity. Tito’s leads here — the brand of competent hospitality. Grey Goose stays close but is consistently a step behind on these non-premium hosting triggers.

A smaller but strategically rich cluster — premium/refined (~15%), smooth-to-drink (~16%), special occasion (~19%) — is where Grey Goose wins outright. Narrow but highly monetizable ground.

Party-vibe, sports-watching, and easy-to-mix (~15–18% each) are contested territory. No brand has locked them down.

Cross-Category Context: "Relaxing at home" is the single largest entry point for total alcohol at ~41% salience, where domestic beer (43%) and wine (41%) dominate, and where RTD cocktails (24%) and THC beverages (22%) are making active inroads. Vodka’s biggest internal occasion is contested before any vodka brand shows up.

How Audience Segments Differ

Age: stable today, exposed tomorrow: Smirnoff’s share nearly doubles from ~11% MMS among 35–44 to ~25% among 65+. Svedka’s pattern inverts: ~6% among 21–34 collapsing to under 2% among 65+. Grey Goose is remarkably stable across ages (15–18%). Our Alcoholic Beverages tracker reframes this: vodka shows the flattest age profile of any spirit. That is a mixed signal — stable in the near term, but a sign vodka lacks a strong generational anchor to hold young drinkers as they bring wider consideration sets into their core occasions.

Income: the premium tier separates: Among $100K+ households, Tito’s jumps to ~16% MMS and Grey Goose holds at ~17%, while Smirnoff drops to ~15%. High-income consumers trade Smirnoff down and Tito’s up. The clearest untapped lever in the data for Tito’s.

Gender: differences are mild within the vodka category: Among vodka brands, gender skews are small — Grey Goose slightly male, Smirnoff slightly female.

Cross-Category Context: The more strategic gender fact is cross-category: vodka is a structurally female-leaning spirit (+3.9pp female share-of-throat) and the most mentally under-defended female position across U.S. alcohol. Every percentage point of mental share vodka does not hold, wine, non-alcoholic, or RTD cocktails can.

What's Blocking Conversion for Vodka Brands

Price is the dominant friction. About 31% of adults say vodka costs more than they’re willing to pay — rising to ~42% among 65+ and ~33% among households under $50K. This single barrier explains both Smirnoff’s mass dominance and Grey Goose’s ceiling. Total-alcohol price friction runs slightly higher at ~35% and also skews older.

Prep and variety friction limits all spirits. Roughly 13% of vodka consumers cite preparation effort and 13% cite limited variety. Across total alcohol, 16% cite prep as a barrier — and RTD cocktails are structurally engineered to solve exactly that. RTDs sit at 79% ever-consumed but only 23% past-four-week penetration: the habit is not formed yet, but the substitution vector is wide open. This is the single most important leading indicator for a vodka portfolio to track.

Availability barriers are small and evenly distributed. No single access barrier exceeds 16%. Vodka is broadly sold; the decision moment, not the shelf, is where brands win or lose.

Product literacy is a long-tail risk. 11% find vodka "harder to choose or understand in-store" — rising to ~14% among 21–34. As Gen Z enters the category, packaging and on-shelf signaling will matter more than they do today.

Why This Matters Now

Defend the female share-of-throat position before chasing new occasions. Vodka is women’s most mentally under-defended category across U.S. alcohol. This is the single highest-leverage recommendation in this memo. Any competitor — inside vodka or outside it — that builds stronger occasion associations for women can peel share away.

The challenge isn’t awareness; it’s attaching brands to specific moments. Major vodka brands are recognized widely but often fail to surface in the contexts consumers care about. The lever isn’t more media weight — it’s linking the brand to specific moments before the moment is claimed by a different category.

Smirnoff should defend the aging mainstream and open a new door. Its strength in 65+ and rural consumers masks real weakness among 35–44 (~11% MMS). Without a credible mid-funnel play for younger households, the brand’s mental availability will erode as the current base ages.

Svedka needs one occasion, not more awareness. Decent awareness (43% aided) but weak mental share (~4%) and limited clear occasion ownership. Pick one occasion — party vibes, high-energy, or easy-to-mix — and go deep, before tequila and RTDs claim the young-adult territory Svedka currently over-indexes on.

Skyy should stop being everywhere and start being somewhere. Broadly middling across most segments and occasions, with no strong ownership signal. The most dangerous position in a category isn’t weakness; it’s indifference. Skyy needs a segment claim before it needs a product claim.

Breadth beats depth — but only if you have both. The next round of vodka share will go to brands that combine Smirnoff-style breadth with Grey Goose-style occasion meaning, and that move fast enough to outpace the RTD, non-alcoholic, and tequila pressure building outside the category.

About this research

Morning Consult conducts over 30,000 daily proprietary surveys in 45 countries covering more than 5,000 brands and 50 economic indicators.

Our category advantage research is aimed at understanding the needs driving consumers in your category — and how your brand can own more of them. This research is built on validated principles of brand-driven growth and powered by Morning Consult’s industry-leading sampling technology.

Measure the true drivers of brand strength

Capture both mental availability (the likelihood your brand comes to mind when consumers face a need or occasion) and emotional closeness (how strongly consumers connect with your brand), benchmarked against competitors.

Uncover Category Entry Points (CEPs)

Directly tied to mental availability, see the specific needs, occasions, and triggers that drive purchase decisions in your category, and how strongly your brand is linked to them.

Pinpoint growth opportunities

Direct investment toward the moments and consumer segments with the greatest potential to grow your brand.

Turn insights into action fast

Get survey results in 4–5 days through a centralized dashboard and short-form memo that equips stakeholders with clear direction on where and how to win.

Learn more

.png)

Why Honda Is One of the Auto Category's Most Structurally Sound Brands

.png)

Crown Royal and Jack Daniel’s Command the Lead Amongst Whiskey Brands