The bottom line up front

Fragrance is a high-frequency category with a low-loyalty problem. Bath & Body Works dominates on mental availability while high-awareness heritage brands like Chanel, Dior, and Calvin Klein sit well below their awareness levels in actual recall at purchase moments. The bottleneck is almost never awareness — it is the gap between being recognized and being thought of when it counts. The brands winning this category have built associations with everyday occasions. The brands losing ground have not.

In this briefing, we use the Category Advantage research framework. A few terms you should know:

- Mental Market Share (MMS) measures a brand’s "mental availability"—how often it comes to mind, compared to competitors, when consumers think of buying in a category

- Category Entry Points (CEPs) are the specific needs, motivations, situations, or feelings that trigger a consumer to consider a product category and the brands within it

- Network Size refers to the average number of distinct usage occasions or buying situations that consumers mentally associate with a brand

The Category Today

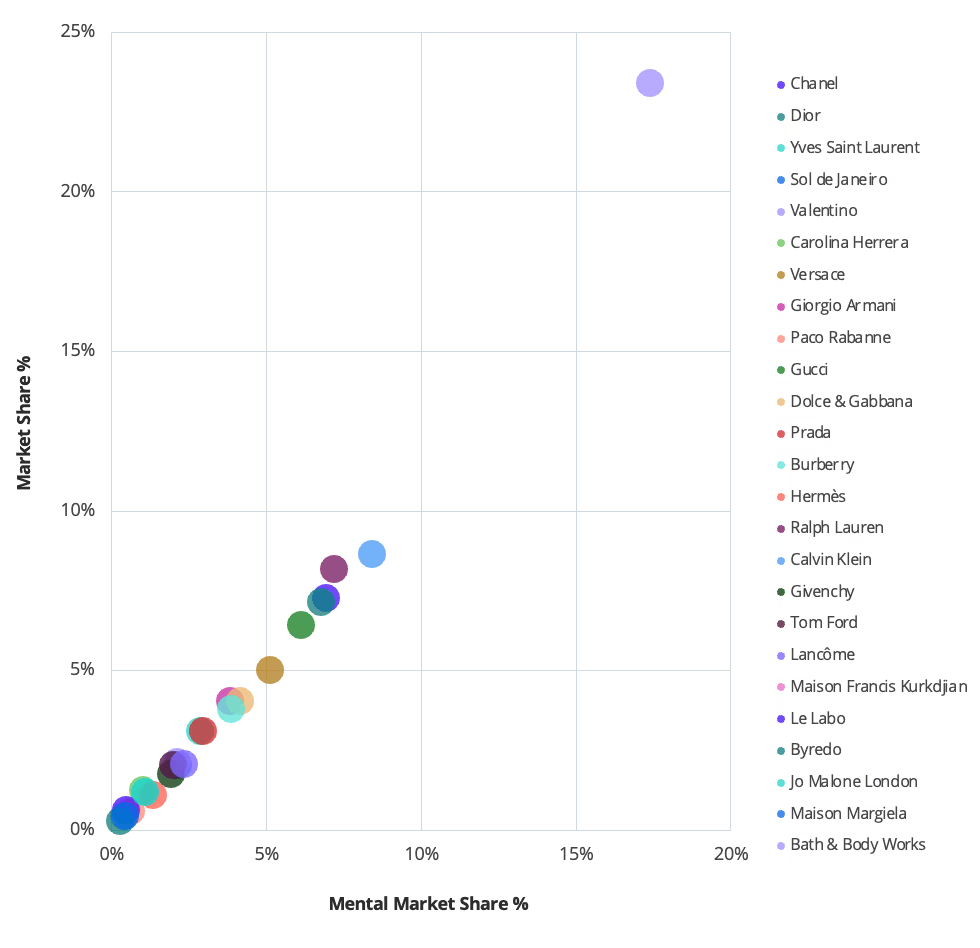

Bath & Body Works has built a category of its own. With ~17% Mental Market Share and a presence at the top of nearly every CEP ranking, Bath & Body Works is the category's default option. Its MMS more than doubles Calvin Klein's (~8%), and its emotional connection score (4.1 on a 1–7 scale) outpaces every fragrance brand in the study. Dominance is especially pronounced among women (26% MMS vs. 9% for men). Every challenger strategy starts from the assumption that Bath & Body Works already owns the front door.

Calvin Klein and Ralph Lauren hold the second tier — but their lead is structural, not emotional. Calvin Klein (~8% MMS) and Ralph Lauren (~7%) are the two closest challengers. Both skew male (CK ~11% MMS among men vs. ~6% women; RL ~10% vs. ~4%) and both have very high aided awareness (~64% and ~60% respectively). But neither clears 3.4 on a 7-point emotional connection scale overall — thought of as reliable defaults rather than desired choices. When a more interesting option surfaces, habit-based loyalty breaks quickly.

Chanel and Dior lead in awareness but trail in mental share — a structural mismatch. Both are known by roughly 62% of U.S. adults, yet MMS sits at ~7% each — nearly equivalent to Ralph Lauren. Chanel over-indexes among women 65+ (~11% MMS) but drops to ~5% among 18–34-year-olds. Dior is more encouraging: ~9% MMS among 18–34-year-olds and 41% purchase likelihood T2B, second-best among fashion houses.

Niche prestige brands carry outsized emotional weight on tiny physical bases. Maison Francis Kurkdjian, Le Labo, and Byredo have minimal aided awareness — MFK ~4%, Le Labo ~5%, Byredo ~3% — yet Mental Penetration among those who know them is extremely high: Le Labo ~74%, MFK ~73%, Byredo ~70%. Emotional connection scores are almost the highest in the study (MFK 4.0), and MFK and Byredo (~29% each) lead the trading-up-to-luxury CEP ahead of every heritage fashion house. The sharpest signal is recency: MFK leads the entire category in recent purchase at ~22% past-4-weeks, with Byredo (~16%) and Le Labo (~14%) also outpacing every major fashion house. These are active repurchase brands. The growth question is whether they can expand their aware base without diluting the intensity that makes them defensible.

Sol de Janeiro is growing faster than its awareness — and that is the tell. Only ~15% of U.S. adults have heard of the brand, yet 60% of those aware have purchased it, and 14% bought it in the last four weeks — on par with Le Labo and ahead of Chanel (6%) or Ralph Lauren (7%). Its MMS among 18–34-year-olds (4.1%) is nearly double its total rate; among parents it reaches 3.9%. Sol de Janeiro is not a low-awareness challenger — it is a category challenger with a lagging awareness metric, and its trajectory makes it the most credible threat to Bath & Body Works's everyday-routine dominance.

Fragrance Audience Context

Economic confidence is eroding. Beauty users have outpaced gen pop on ICS throughout Oct 2025–Apr 2026, but the gap has been narrowing since December. The ~43% who cite price as a barrier is a leading indicator — not a current spending constraint, but a signal that value framing matters more in 2026 than it did in 2024.

This audience skews Millennial and parental. Millennials +8pp vs. gen pop, Gen Z +5pp, parents +14pp.

Media reach runs through TikTok, Pinterest, and Snapchat. TikTok at 74% (+16pp vs. gen pop), Pinterest 66% (+20pp), Snapchat 60% (+19pp). Social is already a fragrance discovery channel — 18% of 18–34-year-olds cite it as a purchase trigger versus 11% overall.

Novelty, status, and premium willingness define this audience. 52% are always looking for the latest trends (+17pp), 42% strive for high social status (+12pp), and 63% will pay a premium for a faster buying experience (+11pp). Friction is especially costly for an audience that is simultaneously aspiration-driven and efficiency-seeking.

The Moments That Matter

Trying a new fragrance (~33%) --the single largest trigger and the most open playing field. No brand dominates: Bath & Body Works leads at 32%, Le Labo and Sol de Janeiro follow at ~29% each. The lack of a clear mental owner makes this the highest-value contested CEP in the study.

Getting ready for a night out or special occasion (~22-23%) -- the category's emotional core. MFK leads the formal occasion CEP at 38%, Le Labo dominates night-out at 36%. Dolce & Gabbana is the only fashion house in the night-out top 3. Chanel ranks #6 on special event, #8 on night out; Dior #7 and #4 respectively — present, but owning nothing.

Replacing a fragrance used for a long time (~22%) -- the loyalty renewal trigger. Bath & Body Works leads again, but Le Labo (~29%) and Byredo (~26%) over-index sharply relative to their awareness. Brands with high repurchase share relative to total awareness are building genuine lock-in, not just trial.

Wearing fragrance every day (~27%) and looking for affordable options (~15%) -- the volume and value occasions. Bath & Body Works dominates both: 48% on the daily routine CEP, 55% on affordability. Sol de Janeiro is the only brand to meaningfully challenge on routine occasions (~32%). Any challenger for this volume tier needs a story that competes on accessibility, not just aspiration.

How Segments Differ

Gender flips the hierarchy; age raises the aspiration ceiling. Bath & Body Works's MMS among women (~26%) is nearly three times its MMS among men (~9%), where Calvin Klein leads at ~11% and Ralph Lauren ~10%. Among 18–34-year-olds, the trading-up trigger reaches 14% salience (vs. 5% among 65+), social recommendation drives 18% of purchase decisions (vs. 5%), and Sol de Janeiro's MMS doubles its total rate. The highest-aspiration buyers are under 35 — and no brand has locked in their loyalty yet.

Income raises the emotional stakes without eliminating price sensitivity. At $100K+ income, the trading-up-to-luxury trigger reaches 14% (vs. 6% for <$50K) and emotional connection to niche brands spikes — MFK reaches 5.0 vs. 4.0 overall. Yet ~46% of this segment still cite price as a barrier, higher than the ~43% total rate. Premium willingness is real but conditional: they will pay more for a product that earns it through discovery and status. They will not pay more for prestige packaging alone.

Why This Matters Now

Diagnose before spending. The most common growth mistake here is buying more awareness for brands already well-known. Chanel is recognized by 62% of U.S. adults. Calvin Klein by 64%. More reach will not solve a mental activation problem. The investment that moves the needle is building associations with the everyday occasions that drive volume — the daily routine, the night out, the seasonal switch — not the formal occasions where these brands already appear but do not own.

For Calvin Klein and Ralph Lauren, the problem is retention, not recruitment. Both have ~56% ever-purchased rates yet ~38% future intent T2B — an ~18pp drop-off among the steepest in the mid-market tier. The question is not how to reach more buyers; it is what makes someone who already bought Calvin Klein choose it again. Without an answer rooted in an occasion the brand owns, media investment will underperform.

Own an occasion, not just a tier. The highest-MMS brands are not the most prestigious — they are the most occasion-versatile. Bath & Body Works wins by showing up at every trigger. MFK wins by owning formal occasions with remarkable intensity. The brands losing ground are positioned at a price tier without a clear occasion home. A brand that owns one high-salience trigger will outperform a brand trying to be everything.

Remove friction before buying more reach. ~43% of buyers cite price as a barrier and ~22% cannot sample before buying — the two largest friction points, both upstream of awareness. For brands above 40% awareness, travel sizes, DTC sample programs, and transparent pricing will generate better returns than equivalent media spend. Versace and Giorgio Armani face a third friction: distribution. At 53% and 46% awareness respectively, they are being blocked by shelf presence, not mental availability.

The under-35 opportunity is open. No brand has locked in mental dominance with younger buyers the way Bath & Body Works has with the total market. Sol de Janeiro's over-index among 18–34-year-olds and Dior's relative strength in this cohort are the early signals. The brands that show up on TikTok and Pinterest with discovery-led messaging and sampling hooks will compound that advantage for decades.

About this research

Morning Consult conducts over 30,000 daily proprietary surveys in 45 countries covering more than 5,000 brands and 50 economic indicators.

Our category advantage research is aimed at understanding the needs driving consumers in your category — and how your brand can own more of them. This research is built on validated principles of brand-driven growth and powered by Morning Consult’s industry-leading sampling technology.

Measure the true drivers of brand strength

Capture both mental availability (the likelihood your brand comes to mind when consumers face a need or occasion) and emotional closeness (how strongly consumers connect with your brand), benchmarked against competitors.

Uncover Category Entry Points (CEPs)

Directly tied to mental availability, see the specific needs, occasions, and triggers that drive purchase decisions in your category, and how strongly your brand is linked to them.

Pinpoint growth opportunities

Direct investment toward the moments and consumer segments with the greatest potential to grow your brand.

Turn insights into action fast

Get survey results in 4–5 days through a centralized dashboard and short-form memo that equips stakeholders with clear direction on where and how to win.

Learn more

Olive Garden Is the Most-Loved and Most-Considered Brand in Dining

The Hotels and Lodging Category Today: Brand Research

.png)