The U.S.-Iran ceasefire collapsed on July 8 after Iran attacked three commercial vessels in the Strait of Hormuz, prompting a second U.S. strike wave hitting 80+ targets. Speaking at the NATO summit, Trump declared the ceasefire "over." Brent crude surged 5.2% to $78/bbl — reversing six weeks of post-ceasefire price relief — as war-risk insurance for Hormuz transits was suspended and tanker rates spiked 40%.

The IMF's July forecast upgrade to 3.2% global growth is now at risk. Energy-importing markets that led Round 1's confidence decline face an immediate reversal; Germany, which had just returned to its pre-war baseline after three consecutive weekly gains, is the most at-risk recovery story in developed markets.

The Global Economy Before The U.S.-Iran Ceasefire Collapsed

Global consumer confidence extended its recovery in the week of July 5, 2026, with the global ICS 4-week MA rising to 98.3 — a +0.6 pt gain and the eleventh consecutive weekly advance since the April 19 trough of 93.2. Extraordinary single-week jumps in Israel (+19.8 pts), Australia (+9.4 pts), Singapore (+6.1 pts) may reflect survey volatility and warrant verification. China reached 166.8 ICS (168.9 MA4). 6 of 43 markets remain more than 10% below their January 2026 baselines.

-

Americas: U.S. ICS edged up to 90.34 (+0.63 WoW), consistent with the flat-to-improving trend of the past month; inflation expectations fell to 4.5%, approaching pre-2022 levels among lower-income households. Canada held flat (~77) as housing correction offsets energy relief. Brazil, Colombia, and Peru lead the region in absolute terms (all above 110), continuing to benefit from commodity demand and trade normalization; Mexico is recovering on near-shoring momentum, but the tariff shock from 2025 continued to weigh on Mexican consumer sentiment.

-

Europe: Germany posted a third consecutive weekly gain (76.78, +2.70 WoW), confirming the energy re-rating thesis — European gas at €34/MWh is now flowing through to household confidence. Spain has fully recovered to its January baseline; France, Italy, and Germany remain the key H2 upside stories as bill relief continues to pass through. UK consumer sentiment held steady, with energy providing particular relief to lower-income households.

-

Asia-Pacific: China rebounded to 166.80 (+4.86 WoW) after two weeks of decline, with Golden Week travel bookings running above 2025 levels, though the sustainability of the bounce is the key question for the July 12 reading. Japan is still waiting on full LNG price pass-through via long-term contract structures. Australia posted the region's largest weekly gain (+9.38 WoW) on delayed energy relief, consistent with its longer-term trend of following trends in China. South Korea is holding in recovery mode as semiconductor exports normalize.

-

MEA: Israel's +19.80 WoW spike to 119.59 — the week's largest global mover — reflects ceasefire confidence deepening and passed outlier review. Gulf leaders Saudi Arabia (152.05) and UAE (149.24) are consolidating at elevated levels. Egypt is benefiting from Suez normalization and strong tourism bookings (+18% vs. 2025). Nigeria and South Africa edged higher on domestic fundamentals; Turkey gradually improved as energy cost relief partially offsets lira weakness and inflation.

What Could Happen to Economies Across the Globe After Ceasefire’s Collapse

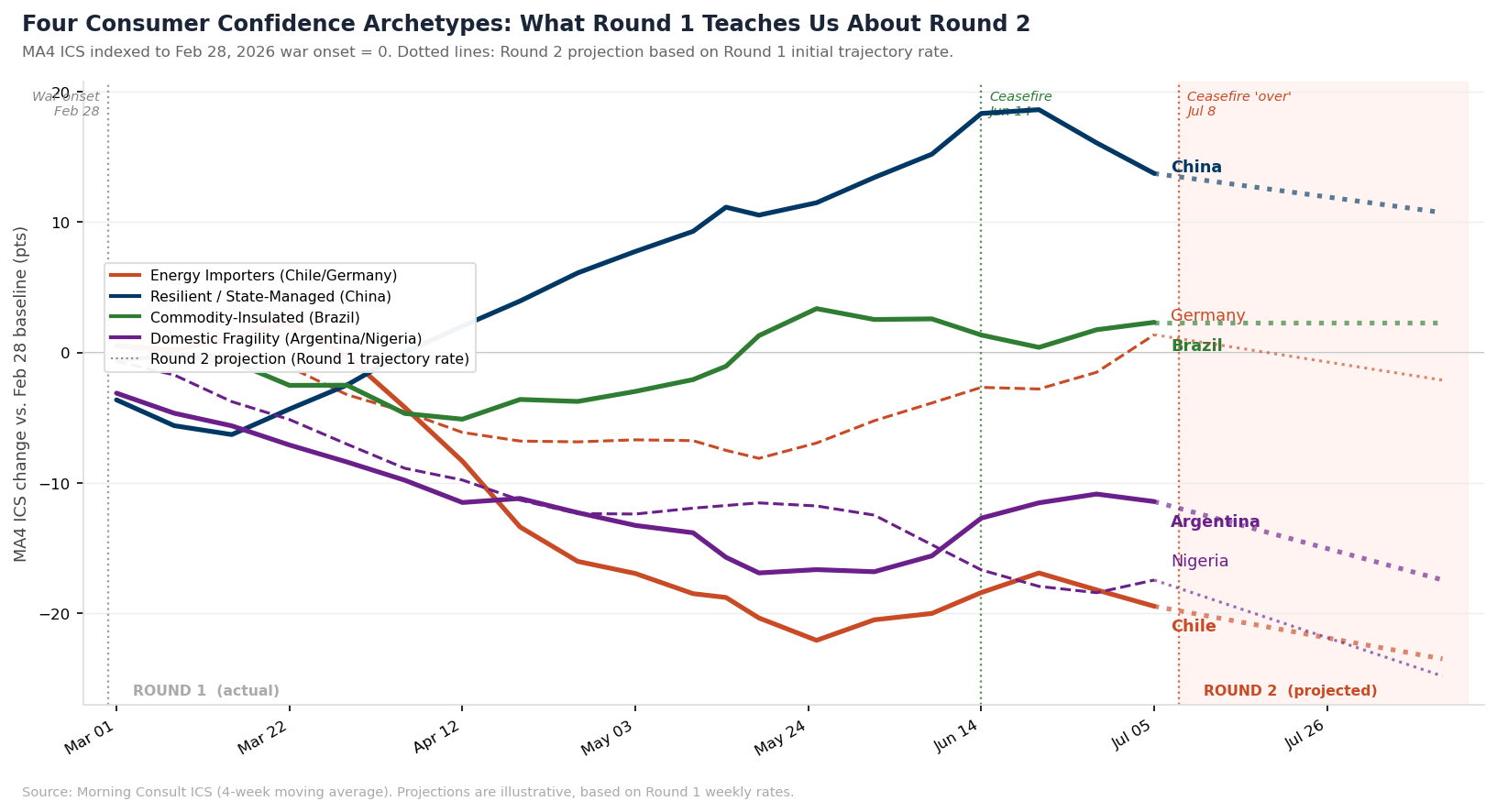

The first round of the Iran-US war and ensuing energy crisis (Feb 28 – Jun 14) sorted global consumer confidence into four distinct archetypes. These patterns are the most reliable forward model for the second round. The chart below shows actual MA4 trajectories indexed to the Feb 28 war onset, with the second round projections (dotted) derived from the first round trajectory rates.

1. Energy Importers (Chile, Germany, Japan, Greece): These countries were hit hardest in Round 1 and then recovered fastest when Hormuz reopened. Chile hit a trough of −22.1 MA4 pts from baseline; Germany declined to −8.1 then fully recovered to +1.4 by Jul 5. In Round 2, expect the same Hormuz transmission channel to operate in reverse — confidence declines within 2–3 weeks as energy prices rise. Germany is the single most at-risk recovery story.

2. Resilient / State-Managed (China): The counterintuitive story of Round 1. China had a brief early dip (−6.3 pts by Mar 15) then surged to +18.3 pts above baseline by the ceasefire — the largest gain of any market globally. State-managed energy prices and overland pipeline alternatives limit Hormuz exposure. The round two expectation for China would be a mild initial decline, followed by a return to its domestic drivers. The key question is whether Golden Week data supports or undercuts the Jul 5 rebound (+4.9 WoW).

3. Commodity-Insulated (Brazil, Colombia): These markets did their own thing during the first round of the energy shock and geopolitical conflict. Brazil is the most idiosyncratic country, which means it tracks its own domestic commodity cycle — iron ore, soybeans, pre-sale crude — not the global energy shock. It dipped briefly in Round 1 then recovered to +2.3 pts above baseline. In Round 2, the insulation mechanism is unchanged: Hormuz disruption benefits commodity exporters through higher prices. Expect Brazil and Colombia to outperform the region again.

4. Domestic Fragility Amplifiers (Argentina, Nigeria): These markets declined throughout Round 1 and did not recover when the ceasefire was announced. Argentina (−11.4 pts vs. baseline) and Nigeria (−17.5 pts) follow their own domestic deterioration tracks — Argentina’s inflation spiral, Nigeria’s naira weakness — that are independent of Hormuz dynamics. The Hormuz shock amplifies existing fragility rather than being the primary driver. In Round 2, expect continued deterioration with no mechanism for recovery tied to the conflict trajectory.

Voters Support Trump’s Iran Action, Until It Impacts Their Wallets

Consumers Say Gas Prices Have Gone Up, and Blame Trump